Campaign of Fear, Uncertainty and Doubt (FUD) About CPEC

An unrelenting campaign of fear, uncertainty and doubt (FUD) about China-Pakistan Economic Corridor (CPEC) has been unleashed in the media in recent weeks. This strategy harkens back to the aggressive marketing techniques used by the American computer giant IBM in the 1970s to fight competition. As in IBM's case, the greatest fear of the perpetrators of FUD is that CPEC will succeed and lift Pakistan up along with rising China.

Fear, Uncertainty and Doubt (FUD):

A definition of FUD that captures its essence is offered by Roger Irwin as follows: "Unable to respond with hard facts, scare-mongering is used via 'gossip channels' to cast a shadow of doubt over the competitors offerings and make people think twice before using it".

A number of articles in western and Indian media have attempted to use FUD against China-Pakistan Economic Corridor. Some Pakistani journalists and commentators, some unwittingly, have also joined in the campaign. As expected, these detractors ignore volumes of data and evidence that clearly contradict their claims.

Part of the motivation of those engaged in FUD against CPEC appears to be to check China's rise and Pakistan's rise with its friend and neighbor to the north. Their aim is to preserve and protect the current world order created by the Western Powers led by the United States at the end of the second world war.

Growing Infrastructure Gap:

Development of physical infrastructure, including electricity and gas infrastructure, is essential for economic and social development of a country such as Pakistan. China-Pakistan Economic Corridor financing needs to be seen in the context of the large and growing infrastructure gap in Asia that threatens social and economic progress.

Rich countries generally raise funds for infrastructure projects by selling bonds while most developing countries rely on loans from international financial institutions such as the World Bank and the Asian Development Bank to finance infrastructure projects.

The infrastructure financing needs of the developing countries far exceed the capacity of the World Bank and the regional development banks such as ADB to fund such projects. A recent report by the Asian Development Bank warned that there is currently $1.7 trillion infrastructure gap that threatens growth in Asia. The 45 countries surveyed in the ADB report, which covers 2016-2030, are forecast to need investment of $26 trillion over 15 years to maintain growth, cut poverty and deal with climate change.

Chinese CPEC Loans to Pakistan:

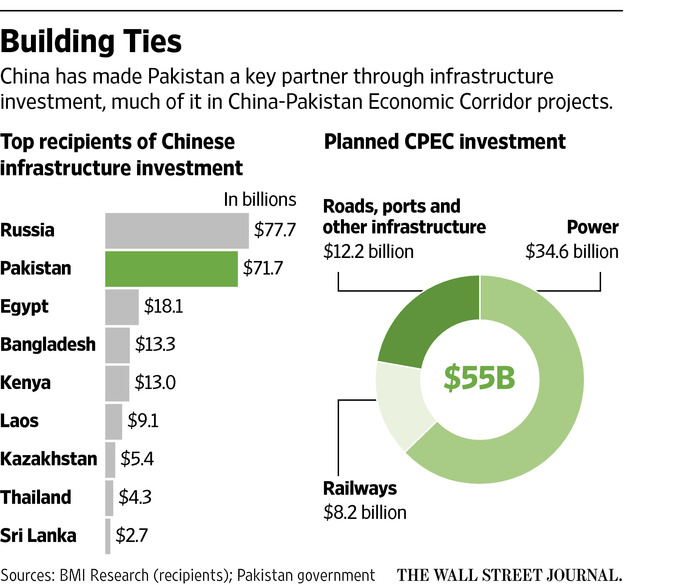

About 80% of the $55 billion of the Chinese money for CPEC is private investment while the rest is composed of soft loans to the government, according to Shanghai Business Review.

The Chinese soft loans for CPEC infrastructure projects carry an interest rate of just 1.6%, far lower than similar loans offered by the World Bank at rates of 3.8% or higher.

Chinese companies investing in Pakistan are getting loans from China's ExIm Bank at concessional rates and from China Development Bank at commercial rates. These loans will be repaid by the Chinese companies from their income from these investments, not by Pakistani taxpayers.

Rising Confidence in Pakistan:

Pakistani economy is already beginning to reap the benefits of the current and expected investments as seen in the 5.2% GDP growth in the current fiscal year, the highest in 9 years.

The World Bank's Pakistan Development Update of May 2017 says that "Pakistan’s economy continues to grow strongly, emerging as one of the top performers in South Asia".

Rapidly expanding middle class and rising demand for consumer durables like vehicles and home appliances attest to the positive impact of CPEC. Consumer confidence in Pakistan has reached its highest level since 2008, according to Nielsen.

US-based consulting firm Deloitte and Touche estimates that China-Pakistan Economic Corridor (CPEC) projects will create some 700,000 direct jobs during the period 2015–2030 and raise its GDP growth rate to 7.5%, adding 2.5 percentage points to the country's current GDP growth rate of 5%.

Fear, Uncertainty and Doubt (FUD):

A definition of FUD that captures its essence is offered by Roger Irwin as follows: "Unable to respond with hard facts, scare-mongering is used via 'gossip channels' to cast a shadow of doubt over the competitors offerings and make people think twice before using it".

A number of articles in western and Indian media have attempted to use FUD against China-Pakistan Economic Corridor. Some Pakistani journalists and commentators, some unwittingly, have also joined in the campaign. As expected, these detractors ignore volumes of data and evidence that clearly contradict their claims.

Part of the motivation of those engaged in FUD against CPEC appears to be to check China's rise and Pakistan's rise with its friend and neighbor to the north. Their aim is to preserve and protect the current world order created by the Western Powers led by the United States at the end of the second world war.

Growing Infrastructure Gap:

Development of physical infrastructure, including electricity and gas infrastructure, is essential for economic and social development of a country such as Pakistan. China-Pakistan Economic Corridor financing needs to be seen in the context of the large and growing infrastructure gap in Asia that threatens social and economic progress.

Rich countries generally raise funds for infrastructure projects by selling bonds while most developing countries rely on loans from international financial institutions such as the World Bank and the Asian Development Bank to finance infrastructure projects.

The infrastructure financing needs of the developing countries far exceed the capacity of the World Bank and the regional development banks such as ADB to fund such projects. A recent report by the Asian Development Bank warned that there is currently $1.7 trillion infrastructure gap that threatens growth in Asia. The 45 countries surveyed in the ADB report, which covers 2016-2030, are forecast to need investment of $26 trillion over 15 years to maintain growth, cut poverty and deal with climate change.

Chinese CPEC Loans to Pakistan:

About 80% of the $55 billion of the Chinese money for CPEC is private investment while the rest is composed of soft loans to the government, according to Shanghai Business Review.

The Chinese soft loans for CPEC infrastructure projects carry an interest rate of just 1.6%, far lower than similar loans offered by the World Bank at rates of 3.8% or higher.

Chinese companies investing in Pakistan are getting loans from China's ExIm Bank at concessional rates and from China Development Bank at commercial rates. These loans will be repaid by the Chinese companies from their income from these investments, not by Pakistani taxpayers.

Rising Confidence in Pakistan:

Pakistani economy is already beginning to reap the benefits of the current and expected investments as seen in the 5.2% GDP growth in the current fiscal year, the highest in 9 years.

The World Bank's Pakistan Development Update of May 2017 says that "Pakistan’s economy continues to grow strongly, emerging as one of the top performers in South Asia".

Rapidly expanding middle class and rising demand for consumer durables like vehicles and home appliances attest to the positive impact of CPEC. Consumer confidence in Pakistan has reached its highest level since 2008, according to Nielsen.

US-based consulting firm Deloitte and Touche estimates that China-Pakistan Economic Corridor (CPEC) projects will create some 700,000 direct jobs during the period 2015–2030 and raise its GDP growth rate to 7.5%, adding 2.5 percentage points to the country's current GDP growth rate of 5%.

|

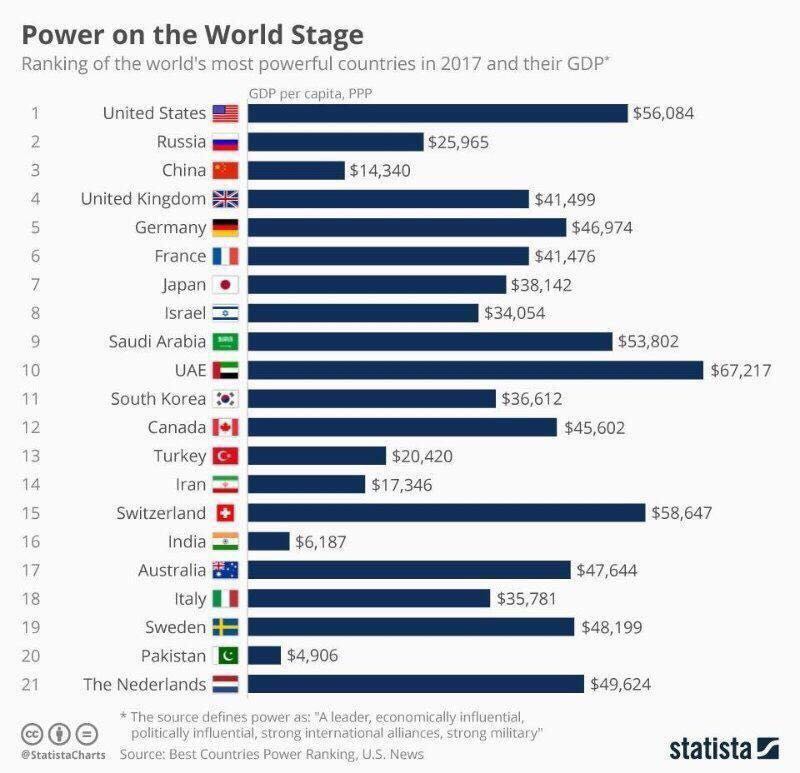

| US News Ranks Pakistan Among World's 20 Most Powerful Nations |

Countering FUD:

Pakistani government should respond to the FUD campaign against CPEC by countering it with facts and data and increasing transparency in how CPEC projects are being financed, contracted and managed. It is particularly important in a low-trust society like Pakistan's where people can be easily persuaded to believe the worst about their leaders and institutions.

Summary:

An unrelenting campaign of fear, uncertainty and doubt (FUD) about China-Pakistan Economic Corridor (CPEC) has been unleashed in the media in recent weeks. This strategy harkens back to the aggressive marketing techniques used by the American computer giant IBM in the 1970s to fight competition. Part of the motivation of those engaged in FUD against CPEC appears to be to check China's rise and Pakistan's rise with its friend and neighbor to the north. As in IBM's case, the greatest fear of the perpetrators of FUD is that CPEC will succeed and lift Pakistan up along with rising China. Their aim is to preserve and protect the current world order created by the Western Powers led by the United States at the end of the second world war. Pakistani government should respond to the FUD campaign against CPEC by countering it with facts and data and increasing transparency in how CPEC projects are being financed, contracted and managed.

Related Links:

Comments

http://www.finance.gov.pk/survey/chapters_17/overview_2016-17.pdf

Per Capita Income in dollar terms has witnessed

a growth of 6.4 percent in FY 2017 as

compared to 1.1 percent last year. The per

capita income in dollar terms has increased

from $ 1,531 in FY 2016 to $ 1,629 in FY

2017. Main contributing factors for the rise in

per capita income are higher real GDP, growth,

low population growth and stability of Pak

Rupee.

------------------

Real GDP growth was above

four percent in 2013-14 and has smoothly

increased during the last four years to reach

5.28 percent in 2016-17, which is the highest in

10 years.

----

The agriculture sector met

its growth target of 3.5 percent, helped by

government supportive policies and by

increased agriculture credit disbursements.

During 2015-16, the agriculture credit

disbursement was close to Rs 600 billion while

during 2016-17, the target was raised to Rs 700

billion. During July-March 2016-17, the

disbursement was observed to be 23 percent

higher as compared to the previous year. These

developments, along with the Prime Minister’s

Agriculture Kissan Package together with other

relief measures have started yielding positive

results.

The large-scale manufacturing output is

primarily based on Quantum Index

Manufacturing (QIM) data, which show an

increase by 5.06 percent from July 2016 to

March 2017. Major contributors to this growth

are sugar (29.33 percent), cement (7.19

percent), tractors (72.9 percent), trucks (39.31

percent) and buses (19.71 percent). High

growth of sugar is based on production of 73.9Million Tons of Sugarcane as compared to 65.5

million tons last year, which represents an

increase by 12.4 percent.

Large Scale Manufacturing growth has picked

up momentum and posted a strong 10.5 percent

growth in the month of March 2017 compared

to 7.6 percent in March 2016. The YoY growth

augurs well for further improvement in growth

during the period under review.

On average, the LSM growth stood at 5.06

percent during July-March FY 2017 compared

to 4.6 percent in the same period last year. The

sectors recording positive growth during JulMar

FY 2017 are textile 0.78 percent, food and

beverages 9.65 percent, pharmaceuticals 8.74

percent, non-metallic minerals 7.11 percent,

cement 7.19 percent, automobiles 11.31

percent, iron & steel 16.58 percent, fertilizer

1.32 percent, electronics 15.24 percent, paper &

board 5.08 percent, engineering products 2.37

percent, and rubber products 0.04 percent.

Pakistan is bestowed with all kinds of resources

which also include minerals. Pakistan possesses

many industrial rocks, metallic and nonmetallic,

which have not yet been evaluated. In

the wake of the 18th Amendment, provinces

enjoy great freedom to explore and exploit the

natural resources located in their authority, with

the result that they are currently undertaking a

number of projects using their own resources,

or in collaboration with the federal government

or with donors to tap and develop these

resources.

The services sector recorded a growth of 5.98

percent and surpassed its target which was set

at 5.70 percent. Wholesale and retail trade

sector grew at a rate of 6.82 percent. The

growth in this sector is bolstered by the output

in the agriculture and manufacturing sectors.

The share of Agriculture, Manufacturing and

Imports in Wholesale and Retail Trade growth

is 18 percent, 54 percent and 15 percent

respectively. The Transport, Storage and

Communication sector grew at a rate of 3.94

percent. Finance and insurance activities show

an overall increase of 10.77 percent, mainly

because of rapid expansion of deposit formation

(15 percent) and demand for loans (11 percent).

Pakistan's Finance Minister Ishaq Dar Friday presented a $50 billion development heavy budget that also promised a seven percent increase in military spending, a growth rate of near 6 per cent and an appeasement for farmers who protested ahead of the budget announcement, clashing with police who used tear gas to disperse them.

The budget offered Pakistan's farmers $6.8 billion in loans, as well as fuel and electricity subsidies.

In poor Pakistan the budget promised $1.15 billion in subsidies, mostly to reduce electricity and fuel costs. In his speech to Parliament Dar said the annual per capita income in Pakistan had increased from $1,334 to $1,629 over the last four years of Prime Minister Nawaz Sharif's government. Tax collection which is notoriously low in Pakistan also increased nearly 80 percent in the same period, he said.

In addition to a seven percent increase in military spending, Pakistan's budget also gave every soldier a 10 percent salary hike for fighting terror. The defense budget was set at $9 billion compared to $8.4 billion last year.

Pakistan's defense budget is not open for debate by Parliament nor does it generally include pensions paid to military personnel. The cost of their pensions comes out of the current budget.

Pakistan has been in a protracted war against terrorists with most battles waged in the tribal regions that border Afghanistan.

Friday's budget was seen as business friendly, offering a 30 percent tax cut to the corporate sector. It also exempts industries from the country-wide rolling power cuts that afflict Pakistanis on a daily basis.

Of the $20 billion plus development budget, Dar said $1.8 billion will go toward financing projects linked to its multi-billion dollar China-Pakistan Economic Corridor scheme that includes a vast array of joint ventures including roads and power plants.

Opposition politicians slammed the budget, with Asad Umar of the Tehreek-e-Insaf (Movement for Justice) party saying it takes from the poor to give to the rich.

"Money is being snatched from the pockets of the poor and middle classes to enhance the wealth of the unproductive elite," Umar said in a statement.

In a country with a literacy rate of 69.5 per cent among men and 45.8 among women, according to the latest CIA country report, the education budget was set at $887 million, considerably less than the sums allocated for defense and development.

The health sector in Pakistan, often bemoaned by many Pakistanis as inadequate, was allocated $126 million according to the figures released by the government.

Pakistan's protesting famers timed their protest hours before Dar presented the budget for the next fiscal year before lawmakers on Friday.

Pakistani TV channels broadcast footage showing riot police dragging farmers away from the scene, as well as protesters throwing stones at the police.

http://www.eastasiaforum.org/2017/03/18/cambodia-sri-lanka-and-the-china-debt-trap/

Sri Lanka’s growing economic engagement with China has also generated concern among scholars and policymakers. One side of the argument posits that China has made a positive contribution to the economic growth of Sri Lanka. China has provided Sri Lanka with over US$5 billion between 1971 and 2012. Most of this has gone into infrastructure development, with China investing US$1 billion into a deep-water port at Hambantota and billions into the Mattala Airport, a new railway and the Colombo Port City Project.

As a small country emerging from civil war, infrastructure is crucial in facilitating Sri Lanka’s trade and foreign investment sectors. The World Bank forecasts that Sri Lanka’s GDP growth is likely to grow from 3.9 per cent in 2016 to around 5 per cent in 2017.

Yet opponents see flaws in the China–Sri Lanka bilateral relationship. First, Sri Lanka has borrowed billions of dollars from China in order to build domestic infrastructure. Sri Lanka’s estimated national debt is US$64.9 billion, of which US$8 billion is owed to China. This can be attributed to the high interest rate on Chinese loans. For the Hambantota Port project, Sri Lanka borrowed US$301 million from China with an interest rate of 6.3 per cent, while the interest rates on soft loans from the World Bank and the Asian Development Bank (ADB) are only 0.25–3 per cent. Sri Lanka is very deep in a debt crisis or ‘debt trap’ as some scholars describe it.

Second, Sri Lanka is currently unable to pay off its debt to China because of its slow economic growth. To resolve its debt crisis, the Sri Lankan government has agreed to convert its debt into equity. But the recent Sri Lankan decision allowing Chinese firms 80 per cent of the total share and a 99 year lease of Hambantota port caused public outrage and violent protests in Sri Lanka. In addition, Chinese firms have been given operating and managing control of Mattala Airport, built by Chinese loans of US$300–400 million, because the Sri Lankan government is unable to bear the annual expenses of US$100–200 million.

According to Brookings Institute visiting fellow Kadira Pethiyagoda, having access to the Hambantota port and Mattala airport provides Beijing with a strategic military position in the event of an Indian Ocean conflict and is also key for its ‘Belt and Road’ initiative. The growing Chinese influence may also compel Sri Lanka to support China’s position on the South China Sea dispute and ‘One China’ policy.

https://www.nationalheraldindia.com/interview/2017/05/17/one-belt-one-road-silk-road-cpec-will-spur-growth-in-asia-says-un-official-china-india-economy

A statement by the (Indian) Ministry of External Affairs (MEA) last week had said the OBOR would create “unsustainable debt burden for communities”. However, Sebastian Vergara, Economic Affairs Officer at the United Nations’ Department of Social and Economic Affairs (DESA), says the project would benefit Asia, in an interview with National Herald.

However, achieving productivity growth must be a government policy priority if India wants to continue to grow above 7%. India must encourage public private partnership (PPP) projects in key sectors, especially infrastructure. Business structural reforms should be vigorously pursued. The health of the public banking sector is a big worry for India, and the government needs to tackle the level of debt with sound policies.

https://www.moodys.com/research/Moodys-Pakistan-shows-strong-growth-and-reduction-in-fiscal-deficits--PR_366262

New York, May 07, 2017 -- Strong growth performance, fiscal deficit reduction and improved inflation dynamics underpin the Government of Pakistan's B3 rating with a stable outlook, says Moody's Investors Service.

At the same time, credit challenges include a relatively high general government debt burden, weak physical and social infrastructure, a fragile external payments position, and high political risk. In particular, the government's very narrow revenue base weighs on debt affordability. Meanwhile, exports and remittance inflows have slowed and capital goods imports have risen, resulting in renewed pressure on the external account.

Moody's conclusions are contained in its annual credit analysis of Pakistan, "Government of Pakistan -- B3 Stable". The analytical factors that are used in its Sovereign Bond Rating Methodology are: economic strength, which is assessed as "moderate"; institutional strength "very low (+)"; fiscal strength "very low (-)"; and susceptibility to event risk "high".

Moody's notes that prospects for growth have improved following Pakistan's successful completion of its three-year Extended Fund Facility (EFF) program with the International Monetary Fund (IMF) in September 2016 and the launch of the China-Pakistan Economic Corridor (CPEC) project in 2015.

Moody's notes that the implementation of the CPEC project has the potential to transform the Pakistani economy by relieving infrastructure bottlenecks, and stimulating both foreign and domestic investment. However, headwinds to further fiscal consolidation and renewed pressure on the external account present downside risks to the rating.

"Since 2013, implementation of economic reforms and increased foreign investment flows have contributed to macroeconomic stability and higher GDP growth. However, government debt remains elevated and pressure on the external account continues. " said William Foster, a Vice President and Senior Credit Officer at Moody's.

The stable outlook represents balanced upside and downside risks to the sovereign credit profile. Support from multilateral and bilateral lenders has bolstered Pakistan's foreign currency reserves and fostered progress on economic reforms. Meanwhile, implementation of the CPEC project has the potential to transform the Pakistani economy by relieving infrastructure bottlenecks, and stimulating both foreign and domestic investment. However, headwinds to further fiscal consolidation and renewed pressure on the external account present downside risks to the rating.

Upward triggers to the rating would stem from sustained progress in structural reforms that would significantly reduce infrastructure impediments and supply-side bottlenecks. This would improve Pakistan's investment environment and eventually aid a shift to a sustained higher growth trajectory. A fundamental strengthening in the external liquidity position and meaningful reduction in the government deficit and debt burden would also be credit positive.

Conversely, Moody's would view a stalling of the government's post-IMF program economic reform agenda, material widening of the fiscal deficit, a deterioration in the external payments position, withdrawal of multilateral and bilateral support, or a more unstable political environment as credit negative.

CPEC: calling the shots

By Yasir MasoodPublished: June 2, 2017

https://tribune.com.pk/story/1425075/cpec-calling-shots/

To counter the nefarious narratives of the critics against CPEC, let’s first understand that the inflow of the funds from China, now estimated to be $62 billion: (a) $36 billion as Chinese investment in power projects which will add up 7,000-11,000 MW to the national grid by 2018. This sum will have no direct financial implications on Pakistan’s external payment obligations and; (b) $26 billion in a Chinese government loan, dedicated to building infrastructure. Since the inflow of funds as loans and FDI has dissimilar financial implications; therefore, a separate evaluation is direly needed to compute some of the major benefits as under.

Pakistan’s economy has severely suffered because of the energy crisis over the last decade or so. A much-needed uptick in power generation under CPEC will help revitalise the worst-affected industrial sectors. And particularly the cotton textile production and apparel manufacturing, which are the country’s largest industries, accounting for about 66 per cent of the merchandise exports and almost 40 per cent of the employed labour force. It will also help rejuvenate the remotely located cottage industry, small size manufacturing, agriculture and mining industry businesses to become commercially viable and contribute its due share of the GDP, on the one hand, and create more job opportunities in the far-flung areas on the other.

It is a misgiving that the Chinese power companies would be availing higher tariff rates. The National Electric Power Regulatory Authority (Nepra) has not mentioned any such concessions or exemptions and has to act according to its jurisdiction to maintain uniformity. Similarly, other regulatory bodies will also look after the environmental hazards, avert abuse of dominant positions, ensure recovery of other levies, implementation of labour laws, and above all, the vibrant and robust courts can swiftly act to protect the constitutional rights of the general public as per laws of the land.

The second part, which will be an interest-bearing loan, that constitutes about 40 per cent of the total $62 billion chunk under the CPEC framework will not overburden Pakistan’s ballooning current and future foreign payment liabilities, as dreaded by some critics unfamiliar with repayment dynamics. Pakistan has been borrowing from the IMF at an interest rate ranging from 5 to 10 per cent just to avert the default on external payments in time. Whereas CPEC loan will be carrying an aggregate interest rate of not more than 1.9 per cent per annum and even below, repayable in a period stretched over 25-30 years and even more.

Reimbursement of the loan with markup, which is estimated to be around $1.5 billion per annum, will start in 2019 and after gradual increase would remain within the range of $4.5 to $5 billion even in the peak years. This additional burden on account of CPEC’s loan would be quite nominal when compared with its eventual upshots — briefly calculated below.

Pakistan’s existing transportation network is quite dilapidated and causing a huge loss of around 3.5 per cent of the country’s annual GDP as estimated by the government. According to the IMF, Pakistan’s total GDP in 2016 was around $285.153 billion of which 3.5 per cent amounts to $9.98 billion. Improvement in the transportation network under CPEC will considerably cut down such losses, thereby reducing Pakistan’s oil import bill and related transport equipment. Similarly, Pakistan’s national exchequer will be earning around $6 to $8 billion a year under toll tax revenue, etc.

Put together, the above two explained sources of income and savings alone will be substantially higher, when matched with the disbursement of loan and debt service liability to China and that too insignificantly spread over a period of 25-30 years and even more.

http://www.arabnews.com/node/1110696

Last week, Pakistan achieved a quiet milestone, returning to the prestigious MSCI Emerging Markets Index after losing its status in 2008. Joining 23 other countries on the index, from high-growth Asian economies to large Latin American and rising Eastern European ones, Pakistan has now returned to the “premier league” of emerging markets.

Long-term, this will mean a steady flow of global capital entering Pakistan’s equities markets. It will also offer a confidence boost for foreign investors. But Pakistanis can be forgiven if they are hardly in a mood to celebrate, as widespread electricity shortages wrack the country once again.

Peshawar residents face cuts of six to eight hours per day, and violent protests broke out in the northwest province of Khyber Pakhtunkhwa over the cuts, leaving at least two dead. Even the commercial metropolis of Karachi has not been spared, losing electricity in several parts of the city last week, prompting protests.

Electricity shortages are bad enough under normal circumstances, but during the holy month of Ramadan — when stomachs are growling, and the need for electricity to cook food ahead of the breaking of the fast becomes even more urgent — it becomes a combustible mix.

For Prime Minister Nawaz Sharif, the electricity shortages present a serious embarrassment for a leader who placed the issue at the center of his election campaign in 2013. Whether or not Pakistan can keep the lights on could determine his future as prime minister.

Enter China. One of the most impactful elements of the much-vaunted, multibillion-dollar China-Pakistan Economic Corridor (CPEC) will be Beijing’s investments in Pakistan energy projects. Last month, Pakistan inaugurated a Chinese-financed, coal-fired power plant in Punjab, completed after 22 months of work, while announcing the launch of a plant in electricity-starved Baluchistan province.

From wind and solar to coal and hydro, China’s energy projects across Pakistan are dizzying in scope and potentially transformative to the future of the South Asian country of some 200 million people. According to the CPEC website, there are at least 18 active projects in various stages of development.

As with all projects, some will materialize and be delivered on time, others will be delayed or fall off the map, but even if China delivers on half of the proposed projects, Pakistan’s future will be, well, brighter.

Numerous studies have demonstrated the direct causal link between access to energy and economic growth. Economists need not have spent so much time constructing graphs and testing the thesis. It is common sense. Imagine an industrial revolution without regular access to energy?

Pakistan has become something of a darling in the emerging-markets investment community of late. Pakistan’s Global X MSCI exchange traded index was up 18 percent over the past 12 months, though it took a sharp dive after officially entering the MSCI Index last week. It seems traders had been buying the rumor, so to speak, and sold the fact.

Over the past three years, Pakistan has issued a successful Eurobond as well as sukuk bonds, heavily oversubscribed by yield-hungry international investors betting on the Pakistan growth story. The World Bank projects a healthy 5.2 percent growth rate for 2017.

Moreover, consumer companies are harvesting growth by targeting the country’s rising middle class. Former governor of the State Bank of Pakistan, Ishrat Husain, told me that companies such as Nestle and Proctor & Gamble are seeing impressive 25-percent rates of return. Some investment strategists are even touting a new post-BRICs (Brazil, Russia, India and China) acronym: VARP (Vietnam, Argentina, Romania and Pakistan).

Ishrat Husain

https://www.dawn.com/news/1313992

The total committed amount under CPEC of $50 billion is divided into two broad categories: $35bn is allocated for energy projects while $15bn is for infrastructure, Gwadar development, industrial zones and mass transit schemes. The entire portfolio is to be completed by 2030.

------

The entire energy portfolio will be executed in the IPP mode —as applied to all private power producers in the country. Foreign investors’ financing comes under foreign direct investment; they are guaranteed a 17pc rate of return in dollar terms on their equity (only the equity portion, and not the entire project cost). The loans would be taken by Chinese companies, mainly from the China Development Bank and China Exim Bank, against their own balance sheets. They would service the debt from their own earnings without any obligation on the part of the Pakistani government.

Import of equipment and services from China for the projects would be shown under the current account, while the corresponding financing item would be FDI brought in by the Chinese under the capital and finance account. Therefore, where the balance of payments is concerned, there will not be any future liabilities for Pakistan.

To the extent that local material and services are used, a portion of free foreign exchange from the FDI inflows would become available. (Project sponsors would get the equivalent in rupees). For example, a highly conservative estimate is that only one-fourth of the total project cost would be spent locally and the country would benefit from an inflow of $9bn over an eight-year period, augmenting the aggregate FDI by more than $1bn annually. This amount can be used to either finance the current account deficit or reduce external borrowing requirements. Inflows for infrastructure projects for local spending would be another $4bn over 15 years.

Taking a highly generous capital structure of 60:40 debt-to-equity ratio for energy projects, the total equity investment would be $14bn. Further, assuming the extreme case that the entire equity would be financed by Chinese companies (although this is not true in the case of Hubco and Engro projects, where equity and loans are being shared by both Pakistani and Chinese partner companies) the 17pc guaranteed return on these projects would entail annual payments of $2.4bn from the current account.

CPEC’s second component, ie infrastructure, is to be financed through government-to-government loans amounting to $15bn. As announced, these loans would be concessional with 2pc interest to be repaid over a 20- to 25-year period. This amount’s debt servicing would be the Pakistan government’s obligation. Debt-servicing payments would rise by $910 million annually on account of CPEC loans (assuming a 20-year tenor). Going by these calculations, we can surmise that the additional burden on the external account should not exceed $3.5bn annually on a staggered basis depending on the project completion schedule.

As a proportion of our total foreign exchange earnings of 2016, this amounts to 7pc. These calculations do not take into account the incremental gains from GDP growth that will rise because of investment in energy and infrastructure. As the loan amounts would be disbursed in the next 15 years and repayments would be staggered, the adding of the entire $15bn to the existing stock of external debt and liabilities is not an accurate representation. The more realistic approach would be a tapered schedule, with $2bn to $3bn getting disbursed in the earlier years and slowing down in the second half.

https://www.reuters.com/article/us-china-silkroad-pakistan-insight-idUSKBN19503Y

By Drazen Jorgic | ISLAMABAD

Last year, Pakistan held informal talks with General Electric, Siemens and Switzerland's ABB to build the country's first high-voltage transmission line. Chinese power giant State Grid committed to building the $1.7 billion project in half the time of its European counterparts – and clinched the deal.

This is a familiar tale in Pakistan and many other countries.

-------------

As China makes its "Belt and Road" initiative – a massive project to connect Asia with Africa and Europe through land and maritime routes – a policy priority for the next decade, Chinese companies are taking the lion's share of infrastructure projects across the region.

Just last year, Chinese firms won project contracts in Belt and Road countries worth $126 billion, state media reported.

In Pakistan, whose geographical position makes it central to Beijing's "Silk Road" plans, contracts have been awarded for projects worth more than $28 billion – all by Chinese companies working together with local firms. More than $20 billion in new investment is likely in the next few years, Pakistan's Planning Minister Ahsan Iqbal told Reuters this week.

Last month, Pakistan's government took out full-page newspaper advertisements on the first China-Pakistan project completed under the plan, a 1,300 mw coal plant that it said was constructed in 22 months, a record time for such a facility. The plant is owned by China's state-owned Huaneng Shandong and the Shandong Ruyi Science & Technology Group.

-------------------------

But two officials at two Chinese state-owned banks that direct government funding, China Development Bank (CDB) and Export-Import Bank of China (EXIM), told Reuters that they have been instructed by the government to favor lending to Chinese firms for Silk Road projects.

The officials also said that the two banks prefer that companies working on infrastructure projects across the region import raw materials or purchase equipment from China.

There is some criticism in Pakistan that the awarding of the contracts to Chinese companies – while speeding up projects – is also costing the country more money.

In the transmission line project deal, for example, General Electric estimated it could make one key part of the line – the converter stations – for about 25 percent less than what State Grid was charging, according to a Pakistani government official and two power sources familiar with GE's projections. By awarding the contract to State Grid, Islamabad paid a higher price, they said.

An official at Nepra, Pakistan's independent energy regulator, said State Grid was also given a tax break not on offer to other investors.

Pakistani government officials declined to comment on tax issues regarding the deal.

China Electric Power Technologies Company Limited (CET), the State Grid subsidiary that will build the line, said the price it asked for was fair. "It's a very reasonable cost," said Fiaz Ahmad Chaudhry, managing director of Pakistan's National Transmission & Despatch Company (NTDC) referring to the overall State Grid contract.

----------------

POWER LINES

The transmission line project was conceived as a government-to-government contract to build a 878-km (545-mile) connection between soon-to-built power plants near the coastal town of Matiari and Pakistan's industrial heartland by the eastern city of Lahore.

According to Pakistani officials, no formal competitive bidding was sought for the project, which was finally awarded in December last year.

but thriving, with demand for their financing and services

growing. But this picture belies a critical need for reinvention

if they are to rise to meet today’s pressing challenges effectively.

In particular, the legacy MDBs—the World Bank, the InterAmerican

Development Bank (IADB), Asian Development

Bank (AsDB), African Development Bank (AfDB), and European

Bank for Reconstruction and Development (EBRD)—

have been slow to adjust to many of today’s realities, starting

with the increasing economic role and growing capability of

their borrowers. For example, their major shareholders have

agreed to only minimal adjustments in corporate governance

systems and leadership selection, creating tensions with major

borrowers who want more voice and influence over their policies

and operations. With age, MDBs have become bogged

down in bureaucracy, increasing delays and raising costs to

borrowers, particularly for major infrastructure projects. Perhaps

in frustration, China and other major borrowers have

taken leadership in creating two new MDBs focused heavily

on infrastructure: the Asian Infrastructure Investment Bank

(AIIB) and the New Development Bank (NDB).

Beyond business-as-usual on

concessional financing. Shareholders should commit to

maintain current levels of concessional support across all

MDBs, implying at least $25 billion in concessional lending

annually over the next decade (and possibly more given

the possible additional amounts the AIIB might provide on

concessional terms). As a growing number of countries graduate

from concessional assistance to non-concessional borrowing

and other forms of engagement with MDBs, this baseline

commitment should allow for increased support in the remaining

poor countries, and for allocation of concessional funding

to countries in crisis and to post-conflict reconstruction,

especially at the World Bank (see Recommendation 4). In

addition, given the expected concentration of poor countries

in Sub-Saharan Africa, there should be a shift in concessional \

-------------

Why the slowness to adapt? One reason is that age and

bureaucratic growth have taken their toll, particularly at the

World Bank, where political pressures and the close scrutiny

of NGOs have affected its operations by making traditional

donors very—and perhaps excessively—risk averse to stories

of corruption, waste, human rights abuses, and environmental

injustices.10,11 In response to these pressures, the legacy MDBs

have gradually become burdened with a proliferation of rules

and processes that are meant to eliminate corruption and

safeguard legitimate aims such as environmental and social

protection, but that often fail to do so effectively or to serve

the institutions’ broader development mission. The result is

widespread borrower frustration with the hassle factor that

increases the costs and delays of major infrastructure projects.

Another reason is that adjustments in the legacy MDBs’

governance have been modest, with the largely western donor

“creditors” dominating the official governance arrangements.

Slow adjustments in governance, especially at the World

Bank, have frustrated the political ambitions of emerging

markets to assume greater leadership at the global level—

through increased capital participation, voting power, and

influence on these and other operational issues that affect

them as borrowers.

The initiative of China and other emerging markets to set

up their own institutions—the AIIB and the NDB—reflects

these two factors.

https://www.cgdev.org/sites/default/files/multilateral-development-banking-report-five-recommendations.pdf

http://www.cetusnews.com/views/BklEbNyNXb?cat=news&title=China-Pushes-U.S.-Aside-in-Pakistan---

By

Saeed Shah

ISLAMABAD—Pakistan’s ruling power structure has long been summed up with the saying “Allah, Army and America.”

China is now staking a claim to supplanting the U.S. with tens of billions of dollars of investment, an embrace that promises Pakistan economic benefits and saddles it with debt—ensuring the relationship will last.

Chinese President Xi Jinping has made Pakistan his flagship partner in a program to spread Chinese-built infrastructure—and Beijing’s sway—across Asia and beyond. Pakistan has so far signed on to $55 billion in Chinese projects, many of them guaranteeing China a high return on its investments and granting tax breaks to Chinese companies.

Former President Barack Obama’s “Asia pivot” is giving way to Mr. Xi’s infrastructure juggernaut, in a model that could be replicated across the region.

“China came in when no one else was willing to invest,” said Commerce Minister Khurram Dastagir. The U.S. missed its chance, he said.

Beijing calls its program “One Belt One Road,” referring to the ancient sea and land Silk Road trade routes that China seeks to revive. Pakistan Prime Minister Nawaz Sharif inaugurated the program’s first big completed project here in late May, a Chinese-built, coal-fired power plant in his home province of Punjab.

China is building roads, railways, power plants and a port, and has lent Pakistan $2 billion in under two years to shore up its foreign-exchange reserves.

A promised $1 trillion Chinese splurge hasn’t yet materialized for many countries. But in Pakistan, $18 billion in projects are under construction in what is known as the China Pakistan Economic Corridor.

The centerpiece is Pakistan’s Arabian Sea port at Gwadar, under expansion and run by a Chinese company to enable trade in goods from China’s southwest.

Pakistan calculates that the Chinese investments will add 2 percentage points to growth in the next few years by providing infrastructure needed to kick-start industrialization.

President Donald Trump has abandoned what was viewed by the Obama administration as a counterbalance to China, a trade deal with nations in the region called Trans Pacific Partnership. An American official said civilian aid to Pakistan, a longtime ally, remained substantial but “getting our message out is a challenge.”

--------

“We want to move away from geopolitics, to geoeconomics, from fighting wars for others,” said Ahsan Iqbal, Pakistan’s planning minister, who oversees the Chinese investment. “Our vision is to place Pakistan as the hub of trade and commerce in this region.”

China’s expenditure isn’t aid. With transport projects, Pakistan incurs debt; power plants come with an obligation for Pakistan to purchase the electricity produced.

Tahir Mashhadi, a senator from the opposition Muttahida Qaumi Movement, compared China to the East India Company, the commercial enterprise that colonized India before the British government took over.

“Here’s the danger: the banks are Chinese. The money is Chinese. The expertise is Chinese. The management is Chinese. The profits are for China. The labor is Chinese,” said Mr. Mashhadi.

Nadeem Javaid, chief economist at Pakistan’s planning ministry, said Pakistan would be paying $5 billion a year to China by 2022, but that the debt should be easy to manage as Pakistani exports rise, electricity prices fall, and toll revenues are generated from trade from China to Gwadar.

“The fears,” he said, “are not genuine.”

Massive Chinese projects actually exacerbate some of them

http://www.economist.com/news/finance-and-economics/21724427-massive-chinese-projects-actually-exacerbate-some-them-pakistans-old-economic

On June 16th the IMF warned of re-emerging “vulnerabilities” in Pakistan’s economy. It praised GDP growth of above 5% a year, but noted missed fiscal targets and a ballooning current-account deficit. The fund’s own projections a year ago for the fiscal year ending this June underestimated this deficit by about half the final total of $9bn. And based on trends in early April it overestimated the fiscal-year-end foreign-exchange reserves by $3bn.

Independent economists point out that, many times before, collapse has come on the heels of an IMF programme’s conclusion. Sakib Sherani, a former government economist, says that to avoid “egg on its face” for cheerleading Pakistan’s economic recovery just months ago, the IMF is slowly changing its story. By the end of 2018, many predict, Pakistan will come begging again. The fund responds that it is “too early to speculate”.

Some of Pakistan’s faltering can be blamed on bad luck, such as a fall in remittances from workers in the Middle East. But mostly it was, as usual, bad policy. Like its predecessors, the PML-N has failed to enact the structural reforms needed to break Pakistan free of its cycle of crises. Barely any goals of the IMF’s programme were met. Bloated, underperforming or, in the case of Pakistan Steel Mills, closed-down publicly-owned enterprises drain millions from the government each month. “Circular” debt, caused by delayed payments along the electricity-generation chain, is swamping the energy sector once more.

Annual exports have declined by 20% in dollar terms since 2013, stymied by an overvalued currency. All this means the government is again borrowing hand over fistfrom local and foreign banks. In some cases the design of the IMF programme itself has added to Pakistan’s woes: by pushing for increased tax revenue above all else, it has allowed the government to clobber the poor with indirect taxes, milk the (few) direct taxpayers even further, and, as ever, ignore the wealthy elites.

-----------

The source of funds is changing even if government recklessness is not. China plans to invest $62bn in Pakistan for a range of projects, particularly power plants, around the 3,000km (1,875-mile) China Pakistan Economic Corridor (CPEC). That could lift Pakistan to more stable prosperity. But paying for the CPEC will not be easy. Unlike loans from the IMF or World Bank, some two-thirds of those taken out so far, for $28bn-worth of early projects, are on commercial terms, with interest high at around 7% a year. When these loans come due, argues Farooq Tirmizi, an emerging-markets analyst, Pakistan will need a bigger bail-out than ever before.

The IMF has concerns about the lack of transparency surrounding Pakistan’s CPEC debts and how it will repay them. Any future fund lending to the country may include conditions that sow discord between the country and its new patron. And with President Donald Trump in charge of America’s foreign policy, there is no guarantee that the old one, America, will prove as generous—in the event of a crisis—as it has in the past.

ARGUMENT

Pakistan Can’t Afford China’s ‘Friendship’

Pakistan's elites think Chinese cash can save the country. They're wrong.

http://foreignpolicy.com/2017/07/03/pakistan-cant-afford-chinas-friendship/

In recent months, the Chinese-Pakistan Economic Corridor (CPEC) has left Pakistanis emboldened, Indians angry, and U.S. analysts worried. Ostensibly, CPEC will connect Pakistan to China’s western Xinjiang province through the development of vast new transportation and energy infrastructure. The project is part of China’s much-hyped Belt and Road Initiative, a grand, increasingly vague geopolitical plan bridging Eurasia that China’s powerful President Xi Jinping has promoted heavily.

Pakistani and Chinese officials boast that CPEC will help address Pakistan’s electricity generation problem, bolster its road and rail networks, and shore up the economy through the construction of special economic zones. But these benefits are highly unlikely to materialize. The project is more inclined to leave Pakistan burdened with unserviceable debt while further exposing the fissures in its internal security.

-----------------

Despite the bold claims made by China and Pakistan, there are many reasons to be dubious about the purported promises of CPEC. There’s already violence all along the corridor. The north-most part of CPEC is the Karakoram Highway (KKH), which gashes through the Karakoram Mountain Range to connect Kashgar in Xinjiang with Pakistan’s troubled province of Gilgit-Baltistan. Xinjiang is in the throes of a slow-burning insurgency by the Muslim Uighur minority against the Communist state. Gilgit-Baltistan, a Shiite-majority polity under the thumb of a Sunni-dominated Pakistan, is part of the above-noted contested territory of Jammu-Kashmir. Here, geology and weather further limit CPEC. The Karakoram Highway, a narrow road weaving through perilous mountains, can’t bear heavy traffic. Expanding the KKH will not be easy. Residents of Gilgit-Baltistan worry about the environmental costs in relation to the few benefits they will enjoy. There have been episodic protests, which the Pakistani government has ruthlessly put down. Meanwhile, Gwador is experiencing a prolonged drought, frustrating the project while the four extant desalination plants remain idle.

In the south, CPEC is anchored to the port at Gwador in Pakistan’s insurgency-riven Balochistan province. The local Baloch people deeply resent the plan because it will fundamentally change the demography of the area. Before the expansion of Gwadar, the population of the area was 70,000. If the project comes to full fruition the population would be closer to 2 million — most of whom would be non-Baloch. Many poor Baloch have already been displaced from the area. Since construction has begun, there have been numerous attacks against Chinese personnel, among other workers.

There’s also the stubborn problem of economic competitiveness. For CPEC to be more competitive than the North-South Corridor that is rooted to the Iranian port of Chabahar, Gwador needs to offer a safer and shorter route from the Arabian Sea to Central Asia. For that to happen, Gwador needs to be connected by road to the Afghan Ring Road in Afghanistan’s Kandahar province, which is under sustained attacks by the Afghan Taliban. Alternatively, a new route could connect Gwador with the border crossing at Torkham (near Peshawar) by traveling up Balochistan, with its own active ethnic insurgency, through or adjacent to Pakistan’s Federally Administered Tribal Areas, which is the epicenter of Islamist terrorism and insurgency throughout Pakistan. It takes great faith — or idiocy, or greed, or all of the above — to believe that this is possible.

https://tribune.com.pk/story/1443447/inclusive-economic-model/

A study of the Silk Road Economic Belt by the Friedrich-Ebert-Stiftung (FES) and the Stockholm International Peace Research Institute (Sipri) has identified potential issues that may negate any benefits the initiative brings.

The study speculates that the Chinese will likely accept or reject projects based on whether they serve the needs of Chinese industry, rather than what they bring to the recipients.

It also suspects that political tensions between different countries may impede the smooth rollout of projects.

Local elites, the study further suspects, may corner the “spoils” from new projects, thereby exacerbating social tensions. It has also expressed fears that labour rights and environmental protection may not be given the attention they deserve.

Therefore, the study recommends that:

The EU put forward a joint consultative mechanism with China to ensure projects are implemented smoothly, by ensuring all stakeholders have a hand in planning and supervision. Official development assistance programmes in BRI recipient countries should, include assistance in project evaluation. Organisations such as the UNDP and the UN Economic and Social Commission (ESC) for Asia should advise recipient countries on the impact and viability of planned projects. BRI loans should not be allowed to breach the debt burden thresholds determined under the World Bank-IMF debt sustainability framework. And finally, the Belt and Road Initiative needs to attract private capital as there are around $8.5 trillion “sitting in cash, waiting for better investment opportunities”. Bringing in private capital would increase the scale of BRI, open it to non-Chinese companies and allow projects to be implemented more efficiently.

It was perhaps in this frame of mind that some of the delegates at the May Belt and Road Forum had called for a rules-based approach, sensitive to the developmental needs of recipient countries. The stakeholders such as the US, the EU, Russia, India and Japan, according to the study, need to coordinate among themselves and engage with China to promote more transparent partnerships.

Meanwhile, the China-Pakistan Economic Corridor (CPEC) continues to bug India. Out of fear of being overwhelmed socio-economically by China’s Road and Belt Initiative (RBI) India seems to have decided to create problems for the initiative. To start with it has decided not to attend any events connected with the BRI Forum.

What India is most worried about, however, is a collection of infrastructure projects under the label of CPEC, currently under construction throughout Pakistan. It traverses territory which India considers to be disputed. China officially claims not to take sides in the Kashmir dispute, but India believes it has done so by finalising CPEC with Pakistan and ignoring India’s position. As well as compromising India’s territorial integrity, CPEC, in India’s view, is raising other concerns about BRI projects.

India’s version on Gwadar port: the seaport has been leased to China until 2059. Chinese companies are operating the port, developing a 1,000-hectare Special Economic Zone nearby, and building an international airport with a Chinese grant of $230 million. These actions are certainly not driven by altruism. They reflect the strategic value to China of access to the Arabian Sea and proximity to energy-rich West Asia. It should be no surprise that Chinese naval submarines have been spotted in Gwadar.

As the CPEC early harvest projects near fruition, detractors are stepping up their propaganda to denigrate the mega project

http://dailytimes.com.pk/opinion/08-Jul-17/denigrating-cpec

As the early harvest projects of CPEC near fruition, detractors are stepping up their propaganda to denigrate the mega project. Christine Fair, of the Foreign Policy magazine has jumped into the fray to disparage CPEC. Christine Fair is an associate professor at the Centre for Peace and Security Studies (CPASS), within Georgetown University’s Edmund A. Walsh School of Foreign Service. Author of the 2014 book Fighting to the End: The Pakistan Army’s Way of War has been criticized for her hawkish rhetoric, riddled with factual inaccuracies, lack of objectivity, and being selectively biased viewpoints. Her pro-drone stance has been denounced, and called "surprisingly weak" by Brookings Institution senior fellow Shadi Hamid. Journalist Glenn Greenwald dismissed Fair’s arguments as "rank propaganda", arguing there is "mountains of evidence" showing drones are counterproductive, pointing to mass civilian casualties and independent studies. Fair’s journalistic sources have been questioned for their credibility and she has been accused of having a conflict of interest due to her past work with U.S. government think tanks, as well the CIA. She has also been rebuked for comments on social media perceived as provocative, such as suggesting burning down Pakistan’s embassy in Afghanistan or asking India to "squash Pakistan militarily, diplomatically, politically and economically." She has been accused of double standards, partisanship towards India, and has been criticized for her contacts with dissident leaders from Balochistan; a link which "raises serious questions if her interest in Pakistan is merely academic."

China constructed the Karakoram Highway across Gilgit Baltistan in 1974. For forty years, the Indian government found no cause for concern, but is now suddenly raising alarm bells with the advent of CPEC

In her latest Op-Ed titled ‘Pakistan can’t afford China’s friendship’ carried by Foreign Policy issue of July 3, 2017, Ms Fair plays to the Indian gallery by claiming that Pakistan has been emboldened by the CPEC to take on India.

Firstly, she conveniently remains oblivious to the fact that India has upped the ante in Occupied Kashmir by killing more than 200 Kashmiri youth and blinding 3,500 children by firing pellet guns at their eyes. To hide its own atrocities against the hapless Kashmiris, India is incessantly violating the ceasefire agreement across the LOC and killing innocent civilians besides staging fake encounters to malign Pakistan. Indian government has formally protested to the Chinese leadership that portions of CPEC traverse through Azad Jammu Kashmir and Gilgit Baltistan, which are disputed territory. Chinese government has responded that CPEC is an economic project and not a strategic one. Moreover, China has invited India to become a part of CPEC to benefit from the mega project as well as address its grievances or misgivings.

The fact is that China constructed the Karakoram Highway across Gilgit Baltistan in 1974. For forty years, the Indian government found no cause for concern, but is now suddenly raising alarm bells with the advent of CPEC.

https://www.nytimes.com/reuters/2017/07/10/business/10reuters-pakistan-lng-exclusive.html

Pakistan says it could become one of the world's top-five buyers of liquefied natural gas (LNG), with Petroleum Minister Shahid Abbasi predicting imports could jump more than fivefold as private companies build new LNG terminals.

Outlining Pakistan's ambitious plans - which, if fully implemented, could shake up the global LNG market - Abbasi told Reuters that imports could top 30 million tonnes by 2022, up from just 4.5 million tonnes currently.

Cheaper than fuel oil and cleaner burning than coal, LNG suits emerging economies seeking to bridge electricity shortfalls and support growth on tight budgets.

(For a graphic on LNG market share by region click http://reut.rs/2uGUu9X)

"Within five years, I don't see any reason why we should not be beyond 30 million tonnes (in annual LNG imports). We will be one of the top five markets in the world," Abbasi said.

That kind of jump would represent one of the fastest growth stories in the energy industry, comparable to what China has done in many commodities - but there are doubts whether Pakistan can achieve its ambitions, given the complexity and cost of expansion projects.

"It's always possible, but seems very difficult as they will need much more (regasification) capacity and downstream pipeline capacity," said Trevor Sikorski at Energy Aspects, a London-based industry market researcher. "There are infrastructural issues and financial issues."

"Still, it is one of the key LNG growth markets, and its demand will help tighten up the market that has threatened to lurch into over supply."

Abbasi said no one took Pakistan seriously after a decade of botched attempts to bring LNG to the country, but this has changed with the construction of new LNG terminals and gas plants. He said foreign suppliers are now arriving in Pakistan - where energy shortages have prompted Prime Minister Nawaz Sharif to promise he'll end the country's frequent blackouts.

"Before, we used to go out to talk to LNG suppliers. Now they're coming to us," Abbasi said.

"(LNG) is really what has saved the whole energy system. It has been a huge success in Pakistan and it will continue," he said after Sharif on Friday inaugurated a new Chinese-built LNG power plant that uses General Electric turbines.

GETTING CONNECTED

Pakistan built its first LNG terminal in 2015 and, after some delays, a second terminal is due to come online in October, doubling annual import capacity to about 9 million tonnes.

A consortium of Exxon Mobil, Total, Mitsubishi, Qatar Petroleum and Norway's Hoegh is expected to decide by September whether to build a third LNG terminal for about $700 million, Abbasi said.

Pakistan has dropped plans to finance up to two more terminals, as private companies have said they would finance these themselves and use Pakistan's existing gas network to sell directly to consumers.

"That's been the real success and that's where the growth will come from," Abbasi said, adding that about 10 million homes are linked to gas connections in Pakistan - a nation of around 200 million.

"In the last four years, we would have added two million additional connections. We are really ramping that up."

If Pakistan achieves its ambitious development goals, it could significantly erode market oversupply, which has helped pull down Asian LNG spot prices by more than 70 percent since 2014 to around $5 per million British thermal units (mmBtu).

The $50 billion China-Pakistan Economic Corridor is a huge opportunity to build academic capacity in Pakistan, say Abdur Rehman Cheema and Muhammad Haris

https://www.timeshighereducation.com/opinion/pakistani-universities-must-capitalise-on-chinese-investment#survey-answer

The China-Pakistan Economic Corridor (CPEC) unveiled by Chinese president Xi Jinping in 2013, is frequently referred to in Pakistan as a potential economic game changer. Now in its first phase of implementation, it will see the Chinese government pump more than $50 billion (£40 billion) into improving transport links and energy cooperation between China and Pakistan.

Hardly any attention has been paid, however, to how this opportunity might be leveraged to build the technological capacity of Pakistan’s universities. And, so far, academics have been conspicuous by their absence from those clamouring for a share of the pie.

There is no question that universities have a lot to offer in terms of economic development. Introduced in the late 1990s, the Triple Helix concept of university-industry-government relationships has transformed the social role of higher education in many developing countries, casting them as central to the transition to a knowledge-based society, whose policies all three players combine to shape. Although it is not easy to implement in countries that lack research universities or global businesses, studies suggest that the approach generally leads to greater scientific productivity, for instance.

Pakistani universities need to capitalise on China’s own desire to shift itself from a symbol of mass production to a knowledge-based economy. They need to align their strategies with Chinese companies’ existing strengths in information technology, railways, manufacturing and energy. And they need to approach both Chinese firms and the Pakistani government to identify the technical skills areas in which the demand for workers can be expected to rise, and implement new diplomas and short courses accordingly.

Networking is also an important tool that can help bring the spheres of government, industry and the academy together. Pakistan’s Higher Education Commission, which regulates all of its universities, should take the lead and help to start this conversation within universities and research centres, incentivising their interaction with existing firms, as well as establishing incubation facilities for new ones on university campuses, including granting them shared access to university facilities.

CPEC also offers an opportunity to address Pakistan’s rampant inequality. In the country’s poorest province, Balochistan, the federal government could help local politicians and tertiary education providers to set up inclusive business incubation centres charged with developing customised, socially useful entrepreneurial approaches. Drawing on the Chinese experience of poverty reduction, such measures could start to build skilled human resources able to contribute to local and national economic development.

For example, developing local expertise in processing copper – which is mined in Balochistan – could help Pakistan to save the cost of importing the metal after the ore is exported to China for refinement.

The Balochistani port of Gwadar, a gateway to the Middle-Eastern and African markets, is one of the nodes of CPEC and will be connected by new road and rail links to the far western Chinese city of Kashgar, in Xinjiang Province. This offers many business opportunities for Pakistani and international businesses, and local universities could both catalyse and benefit from this if they set up business research excellence centres aimed at helping to improve the quality of the goods and services to be exported.

https://www.thenews.com.pk/latest/217062-Cultural-Caravan-to-travel-in-three-segments-of-CPEC

Chinese and Pakistani artists, eight from each country, will travel in a cultural caravan in three segments of the China Pakistan Economic Corridor (CPEC), each segment spanning a maximum of ten days’ duration.

“Creative Caravan of artists, musicians and film makers from China and Pakistan traversing the CPEC and documenting Art and Culture en-route,” said PNCA officials.

The Silk route has played a significant role in the culture and economy of the region through the history.

Its visionary transformation into CPEC will be seen as the most powerful engine of change, development, progress and economic turnaround for the entire region.

According to schedule the first segment will undertake the Western Passage covering route from Peshawar to Gwadar.

The second segment will take the Eastern Passage from Karachi to Islamabad while also taking detour between Eastern Western and Central Passages.

The third segment will cover Northern Passage starting from Kashgar and culminating at Islamabad.

Timings of the three segments of the caravan will be decided keeping climatic and other factors in mind.

The film makers will have all their equipment including editing systems with them so they can continue editing their films and also engage local talent in the process of filming and editing.

The painters and photographers will be encouraged to engage with local enthusiasts in creative processes by sharing their knowledge and skills with them and also letting them to take pictures and paint images.

The musicians will not only document local folk music but also perform at different places and interact with local musicians.

Published on September 6, 2017

LikeCPEC Fears and My Response

Hamza Orakzai

https://www.linkedin.com/pulse/cpec-fears-my-response-hamza-orakzai

1. 91% of the income from Gwadar Port goes to the Chinese and 9% to Pakistan.

Reply: Can you kindly point out what's wrong with this model especially when all the liabilities and investments lie at their end? In past 7 decades, not only our government has failed to develop the port but also ignored the importance of its geostrategic location, and currently, doesn't have the resources to develop it even if they want to for next 3 decades or so. Every Pakistani still gets to use the port and enjoy the benefits from its development. The port is a window to the economic activity it will generate in the country.

2. Chinese companies get preferential treatment and tax exemptions (making it impossible for local companies to compete and opens the Pakistani market for a commercial invasion)

Reply: The statement is completely misleading. Only CPEC projects get tax exemptions, mainly in the power sector, because we are in dire need to mitigate the losses due to the energy crisis in Pakistan. Moreover, tax exemption also drives down the cost of building these strategic projects, which results in lower tariffs and repayments.

(Impossible is a strong word. Construction companies in Pakistan are working at their full capacity, turning down projects due to output issues. Commercial Invasion? I think mentioning special economic zones would be more relevant since the argument of building infrastructure has no correlation with the commercial viability of businesses.)

3. Money for the road network comes from Pakistan (so we're paying for the roads China will use to export stuff to us and the world)

Ans: Let me break the statement into 2 parts:

1) The Road; 2) The Money

1) The Road: The roads built under CPEC will be the property of National Highway Authority and will generate revenue through the toll tax. Moreover, as a Pakistani, will you want strategic roads in the country to be the property of a foreign country?

2) The Money: These projects are being built on Engineering-Procurement-Construction+Finance (EPC+F) Model. Finance comes from China and our government takes it as a concessionary loan. Same as ADB model. But the difference is that Chinese companies are mandated to complete these grand projects within 24-36 months. There needs to be open bidding for these projects, but then again, it will push the timeline of the CPEC to 30 years instead of 15 years.

4. Of the original $50b, over $30b was loans to build power plants for which we'll pay a) interest to Chinese banks b) exorbitant profits to Chinese companies who will build and supply to these plants c) guaranteed profits to the Chinese companies that will operate and own these plants d) backed by sovereign guarantee

Ans: This figure is completely incorrect. All the power projects under CPEC are BOOT (Build-Operate-Own-Transfer) basis which means that investment, loans, and liabilities are all the investor problems. Our problem is to pay for the electricity they produce. No loan has been acquired so far by the government of Pakistan for energy projects.

a) We have nothing to do with the interest rates.

b) Getting a payback for what you invested is a very fair request so don't know what's wrong with it?

c) Guaranteed profits because we have PKR 800 billion in circular debt? Why would anyone even want to invest? Would you?

d) Same as above.

5. We're making commitments to buy electricity at over 8 cents from coal-based plants and India is buying solar electricity at 4 cents (solar price is crashing every year). This will make our manufacturing uncompetitive for the next 15 years or longer.

Ans: We have a problem in this argument. First, we are comparing apples to oranges. The feed-in tariff for coal power plants is around PKR 8/Kwhr in India as well. Although it's a lengthy discussion,

ISHRAT HUSAIN

https://www.dawn.com/news/amp/1357043

The Chinese have voiced concerns regarding negative CPEC talk, security and red tape.

Under its One Belt One Road Initiative announced in 2013, China is planning to invest more than $1 trillion in 60 countries all over the world to establish six different corridors. The receptivity in other countries to this proposal has been anything but enthusiastic; however, some Chinese friends are puzzled by the sceptical and negative reactions from certain quarters in Pakistan expressed in the media, particularly on social media. This comes to them as a surprise because of the long uninterrupted record of strong bilateral relations between the two countries that were not even affected by changes in political leadership in either country. CPEC is the first project of its kind to foster economic cooperation on a massive scale for building large infrastructural projects in Pakistan.

Although realising that there are some external forces hostile to this initiative, Chinese analysts and participants are concerned about what they see as the misrepresentation of facts by many Pakistanis. It is not obvious to them as to what purpose is served by raising doubts and fears about CPEC in the minds of the Pakistani population. The aspersions being cast on the motives of the Chinese, such as the analogy with the East India Company or Pakistan becoming a satellite of China, are very unnerving: external detractors of CPEC pick up these reports and after bundling them as ‘risks’ of CPEC to Pakistan, disseminate them widely.

The Chinese argue that the IPPs have been a policy instrument for investment in Pakistan’s energy sector for a very long time. When the country was facing serious energy shortages no one else came to Pakistan’s rescue and invested in the sector. Now that China has come forward with a planned investment of $35 billion or 70 per cent of the total CPEC allocation under the same policy, questions are being raised.

Had it involved extraction of natural resources from Pakistan for the benefit of the Chinese, this criticism would have been justifiable. On the contrary, the benefits of this investment would be exclusively appropriated by Pakistan’s industries and households that would no longer face load-shedding while the country would record a 2pc annual rise in GDP growth.

Chinese state-owned companies, designated by the Chinese government based on their expertise and experience, are executing the projects with loans provided by government-owned banks on concessional terms both in tenor and pricing. In several projects, Chinese and Pakistani companies have entered into joint ventures. The repatriation of profits and debt-servicing in foreign exchange arising out of these obligations would become possible after an increase in the volume of exports as a result of the Chinese-Pakistani joint ventures relocating their industries to the Gwadar Free Economic Zone and the nine industrial zones to be established under CPEC.

In the opinion of some, the negative feelings can have unintended adverse consequences for the personal security of Chinese nationals working on these projects, particularly in some sensitive areas of Balochistan. Some elements unhappy with the Pakistani state and government and possibly acting at the behest of foreign powers hostile to CPEC appear to have created conditions in which the murders and kidnappings of Chinese nationals that were almost non-existent have begun to take place. Our interlocutors were grateful for the new division being raised by the Pakistan Army for protection of the Chinese; but the security risk is raising premiums for relocation to some of the vulnerable areas.

Abbasi to impose fresh curbs on luxuries in effort to avoid devaluing rupee

https://www.ft.com/content/a495b148-a1d2-11e7-9e4f-7f5e6a7c98a2

Please use the sharing tools found via the email icon at the top of articles. Copying articles to share with others is a breach of FT.com T&Cs and Copyright Policy. Email licensing@ft.com to buy additional rights. Subscribers may share up to 10 or 20 articles per month using the gift article service. More information can be found at https://www.ft.com/tour.

https://www.ft.com/content/a495b148-a1d2-11e7-9e4f-7f5e6a7c98a2

Pakistan plans to tighten curbs on luxury imports to ward off a foreign currency crisis without devaluing the rupee, Shahid Khaqan Abbasi, the prime minister, has said.

Mr Abbasi said he would rather place further controls on imports in an effort to preserve fast-dwindling foreign reserves than allow the rupee to fall against other currencies.

Some experts believe Pakistan will have to request another bailout from the International Monetary Fund within a year.

In March, the Pakistani government made it harder to import non-essential items such as vehicles, mobile phones, cigarettes and jewellery by insisting buyers put down 100 per cent of the cash upfront.

The measure drew criticism that it would encourage people to trade instead on the black market. The IMF said it had been told by Pakistani officials that the restrictions would be removed within a year but Mr Abbasi told the FT his government was planning to impose more.

“We can put regulatory duties on certain items, especially luxury finished goods, that’s possible,” he said. “We probably will do more of that, yes definitely, to discourage imports.

“Currency devaluation is not on the table, it’s not. A lot of people thought it was . . . [but] it is important to have stability for the rupee,” said Mr Abbasi.

Pakistan is running out of foreign currency as exports and payments from Pakistanis abroad fall while imports rise.

The central bank had $14.3bn of foreign reserves as of September 15, according to the most recent data — enough to cover exports for about three months. That is down from a high of $18.9bn last October.

Pakistan has been importing more than it exports for some time, but the problem has been exacerbated by having to buy Chinese supplies for projects as part of the $55bn China-Pakistan Economic Corridor.