Time to Sell India Short and Go Long on Pakistan?

Is it time to sell India short and go long on Pakistan?

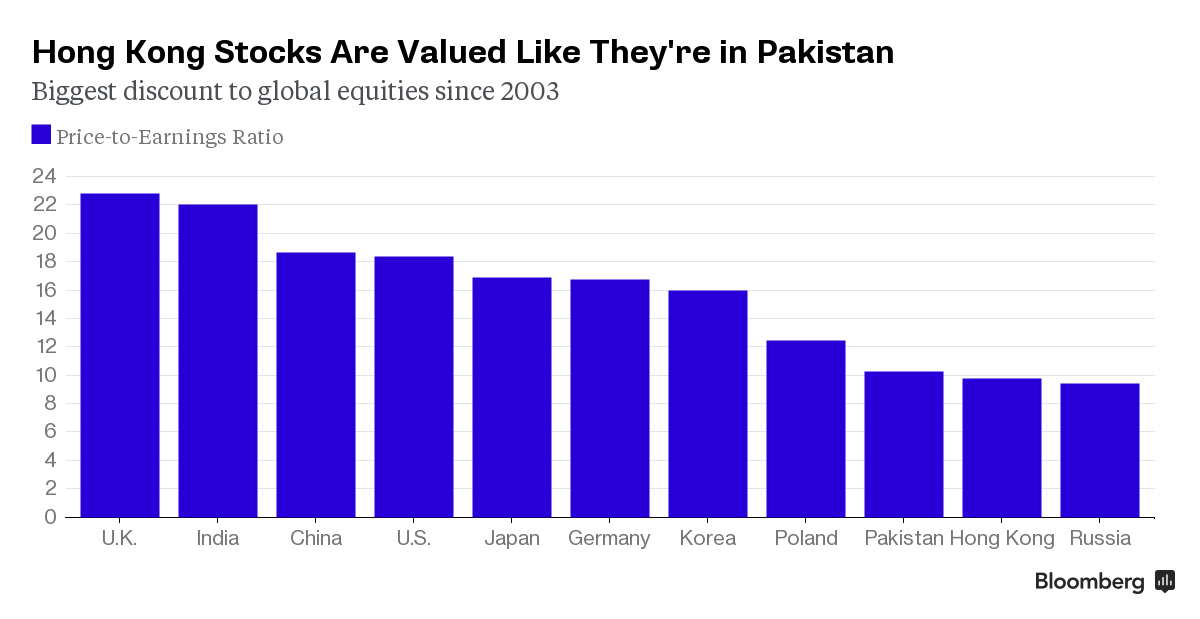

Indian shares are highly overvalued while Pakistan and Hong Kong shares are trading at very attractive valuations, according to latest data published by Bloomberg. The Indian shares listed in Mumbai are trading at nearly 22 times earnings, more than twice the price-earnings multiples of Karachi and Hong Kong listed stocks.

Hong Kong's Hang Seng benchmark gauge for $4.3 trillion of shares was valued at 9.8 times reported earnings on Thursday, a 44 percent discount to the MSCI All-Country World Index, according to Bloomberg. That’s the cheapest level among developed markets worldwide and compares with a multiple of 10.2 for Pakistan’s KSE 100 Index. Russia’s Micex has the lowest valuation among major markets, trading at about 9.5 times profits.

Talking about Pakistan, Charlie Robertson, London-based chief economist at Renaissance Capital Ltd. told Bloomberg that “It (Pakistan) is the best, undiscovered investment opportunity in emerging or frontier markets...What’s changed is the delivery of reforms -- privatization, an improved fiscal picture and good relations with the IMF.” Pakistan is a reform story like neighboring India’s, but only better, Renaissance’s Robertson added.

The massive Chinese commitment to invest $46 billion in Pakistan's energy and infrastructure projects as part of China-Pakistan Economic Corridor has added to the excitement about Pakistan's brightening prospects.

China-Pakistan Economic Corridor (CPEC) is highly strategic for both China and Pakistan. It is expected to dramatically boost investment and trade activity in Pakistan via 29 industrial parks and 21 mining zones along the western, central and eastern routes.

Spurred by Chinese investment, the smart money is taking notice of Pakistan as an attractive investment destination. The investors are looking at the fact that Pakistani stocks have been outperforming both emerging and frontier markets for several years. The benchmark index of the Karachi Stock Exchange (KSE100) is up more than 20% in the last 12 months, according to NASDAQ.com.

Pakistani Shares in 2015:

After a dismal March, MSCI Pakistan rebounded strongly this month, returning 9.1% so far. In April, the iShares MSCI Frontier 100 ETF (FM) rose 4.3%, the WisdomTree India Earnings Fund (EPI) dropped 1.2%, the iShares MSCI India ETF (INDA) fell 1.9%, according to Barron's Asia.

KSE-100 Performance:

In 2014, the KSE-100 Index gained 6,870 points thereby generating a handsome return of 27% (31% return in US$ terms), making Pakistan's KSE world's third best performing market. Total offerings in the year 2014 reached 9 as compared to 3 in the year 2013. After a gap of seven years, Rs 73 billion were raised through offerings in 2014 as compared to a meager Rs 4 billion raised in 2013. Foreign investors, that hold US$ 6.1 billion worth of Pakistani shares -which is 33% of the free-float (9% of market capitalization)-remained net buyers in 2014.

Pakistani Shares Valuation:

Even after outperforming both emerging and frontier market indices, Pakistani shares can be bought at deep discounts which make them very attractive, according to Renaissance Capital’s chief economist Charles Robertson. MSCI (Morgan Stanley Composite Index) Pakistan trades at only 8.4 times forward earnings, a 17% discount to MSCI Frontier Markets. For comparison purposes, fellow frontier south Asia markets Sri Lanka and Bangladesh trade at 13.4x and 21.4x respectively. India, included in the emerging market index, trades at 16.8 times.

Key Sectors:

Chinese investment in energy and infrastructure will help stimulate all sectors of Pakistani economy. But the sectors benefiting most from the $46 billion investment will likely include banks, energy and building materials, the sectors which are the favorites of Pakistani billionaire investor Mian Mohammad Mansha.

Being close to the ruling Sharif family makes Mansha the ultimate insider. Beyond his investments in banking, cement, energy and textiles, Mansha is also starting to invest in consumer products sector benefiting from rising incomes, growing middle class and increasing jobs created in Pakistan by the massive Chinese investment. Mansha owns a big chunk of Muslim Commercial Bank (MCB) share. He has recently been pumping more money into energy, cement and dairy businesses. Mansha's DG Khan Cements has announced plans to build a $300 million cement plant near Karachi. In additions, his Nishat Dairies has imported thousands of dairy cows for a dairy farm in Lahore.

Summary:

The $46 billion Chinese investment in energy and infrastructure has brought attention to tremendous investment opportunities in Pakistan, a nation of nearly 200 million people with rising middle class and growing consumption. Pakistani military's recent successes against the terrorists and China's massive investment commitments are expected to boost investor confidence in the country. Higher confidence will help draw other significant investors to invest in Pakistan over the next several years.

Related Links:

Haq's Musings

China Deal to Set New FDI Records in Pakistan

Post Cold War Realignment in South Asia

Haier Pakistan to Expand Production From Home Appliances to Cellphones, Laptops

Pakistan Bolsters 2nd Strike Capability With AIP Subs

3G, 4G Rollout in Pakistan

Pakistan Starts Manufacturing Tablets and Notebooks

China-Pakistan Industrial Corridor

US-Pakistan Ties and New Silk Route

Indian shares are highly overvalued while Pakistan and Hong Kong shares are trading at very attractive valuations, according to latest data published by Bloomberg. The Indian shares listed in Mumbai are trading at nearly 22 times earnings, more than twice the price-earnings multiples of Karachi and Hong Kong listed stocks.

|

| Source: Bloomberg |

Hong Kong's Hang Seng benchmark gauge for $4.3 trillion of shares was valued at 9.8 times reported earnings on Thursday, a 44 percent discount to the MSCI All-Country World Index, according to Bloomberg. That’s the cheapest level among developed markets worldwide and compares with a multiple of 10.2 for Pakistan’s KSE 100 Index. Russia’s Micex has the lowest valuation among major markets, trading at about 9.5 times profits.

Talking about Pakistan, Charlie Robertson, London-based chief economist at Renaissance Capital Ltd. told Bloomberg that “It (Pakistan) is the best, undiscovered investment opportunity in emerging or frontier markets...What’s changed is the delivery of reforms -- privatization, an improved fiscal picture and good relations with the IMF.” Pakistan is a reform story like neighboring India’s, but only better, Renaissance’s Robertson added.

The massive Chinese commitment to invest $46 billion in Pakistan's energy and infrastructure projects as part of China-Pakistan Economic Corridor has added to the excitement about Pakistan's brightening prospects.

|

| CPEC Projects Map |

China-Pakistan Economic Corridor (CPEC) is highly strategic for both China and Pakistan. It is expected to dramatically boost investment and trade activity in Pakistan via 29 industrial parks and 21 mining zones along the western, central and eastern routes.

This (China's $46 billion investment in Pakistan) can not be purely politically driven. Beijing is commercial: CEO’s, not think tank intellectuals, travel with politicians. Barron's Asia

Spurred by Chinese investment, the smart money is taking notice of Pakistan as an attractive investment destination. The investors are looking at the fact that Pakistani stocks have been outperforming both emerging and frontier markets for several years. The benchmark index of the Karachi Stock Exchange (KSE100) is up more than 20% in the last 12 months, according to NASDAQ.com.

Pakistani Shares in 2015:

After a dismal March, MSCI Pakistan rebounded strongly this month, returning 9.1% so far. In April, the iShares MSCI Frontier 100 ETF (FM) rose 4.3%, the WisdomTree India Earnings Fund (EPI) dropped 1.2%, the iShares MSCI India ETF (INDA) fell 1.9%, according to Barron's Asia.

|

| Source: Economist Magazine |

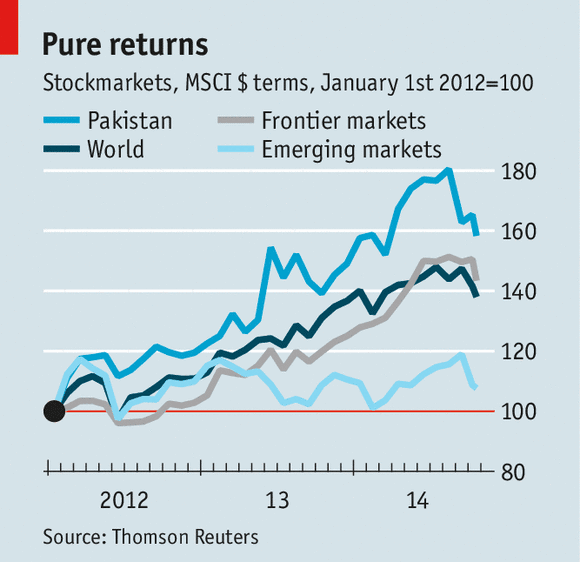

In 2014, the KSE-100 Index gained 6,870 points thereby generating a handsome return of 27% (31% return in US$ terms), making Pakistan's KSE world's third best performing market. Total offerings in the year 2014 reached 9 as compared to 3 in the year 2013. After a gap of seven years, Rs 73 billion were raised through offerings in 2014 as compared to a meager Rs 4 billion raised in 2013. Foreign investors, that hold US$ 6.1 billion worth of Pakistani shares -which is 33% of the free-float (9% of market capitalization)-remained net buyers in 2014.

Pakistani Shares Valuation:

Even after outperforming both emerging and frontier market indices, Pakistani shares can be bought at deep discounts which make them very attractive, according to Renaissance Capital’s chief economist Charles Robertson. MSCI (Morgan Stanley Composite Index) Pakistan trades at only 8.4 times forward earnings, a 17% discount to MSCI Frontier Markets. For comparison purposes, fellow frontier south Asia markets Sri Lanka and Bangladesh trade at 13.4x and 21.4x respectively. India, included in the emerging market index, trades at 16.8 times.

Key Sectors:

Chinese investment in energy and infrastructure will help stimulate all sectors of Pakistani economy. But the sectors benefiting most from the $46 billion investment will likely include banks, energy and building materials, the sectors which are the favorites of Pakistani billionaire investor Mian Mohammad Mansha.

Being close to the ruling Sharif family makes Mansha the ultimate insider. Beyond his investments in banking, cement, energy and textiles, Mansha is also starting to invest in consumer products sector benefiting from rising incomes, growing middle class and increasing jobs created in Pakistan by the massive Chinese investment. Mansha owns a big chunk of Muslim Commercial Bank (MCB) share. He has recently been pumping more money into energy, cement and dairy businesses. Mansha's DG Khan Cements has announced plans to build a $300 million cement plant near Karachi. In additions, his Nishat Dairies has imported thousands of dairy cows for a dairy farm in Lahore.

Summary:

The $46 billion Chinese investment in energy and infrastructure has brought attention to tremendous investment opportunities in Pakistan, a nation of nearly 200 million people with rising middle class and growing consumption. Pakistani military's recent successes against the terrorists and China's massive investment commitments are expected to boost investor confidence in the country. Higher confidence will help draw other significant investors to invest in Pakistan over the next several years.

Related Links:

Haq's Musings

China Deal to Set New FDI Records in Pakistan

Post Cold War Realignment in South Asia

Haier Pakistan to Expand Production From Home Appliances to Cellphones, Laptops

Pakistan Bolsters 2nd Strike Capability With AIP Subs

3G, 4G Rollout in Pakistan

Pakistan Starts Manufacturing Tablets and Notebooks

China-Pakistan Industrial Corridor

US-Pakistan Ties and New Silk Route

Comments

Infina Finance Ltd., a Mumbai-based $190 million hedge fund, has turned the most bearish in a year on India’s stock market and will short if it rallies further.

“Right now we have the lowest net longs than we had in the last 12 months,” Venkat Subramanian, Infina chief executive officer, said in an interview. “If the market goes up any further, I would become net short.”

The long-short equity fund, which counts billionaire Uday Kotak and Kotak Mahindra Bank Ltd. among investors, is expecting a correction as foreigners allocate money to other regions and stock valuations become expensive. Indian equities have rallied as Prime Minister Narendra Modi pledged to revive investments and manufacturing while curbing graft after being swept into office a year ago. The economy grew by 7.5 percent in the January-March period, faster than the previous quarter’s 6.6 percent rate.

“Current market sentiment is very bullish, but it is possible that earnings expectations won’t be met” as it will take at least another 15 months before the government’s actions can bolster company earnings, Subramanian said. “Companies in consumer goods, telecommunication services and auto-components could be the space where significant disappointments could happen.”

The fund, which has the capacity to use leverage though it’s not employing it, has returned about 16 percent every year since its inception in 2008, according to Subramanian.

Earnings Expectations

Earnings for companies in the benchmark S&P BSE Sensex Index are estimated to grow about 31 percent in fiscal 2016. That compares with about 13 percent for those in the MSCI Emerging Markets Index.

The Sensex’s valuation of 15.4 times projected 12-month earnings is about 30 percent higher than the MSCI Emerging Markets Index. The benchmark closed 0.9 percent higher at 28,020.87 points. It has added 1.9 percent this year.

“Things are improving on the domestic front as this government has started doing things which will start showing up in company earnings in 15 to 18 months,” Subramanian said. “But the market has already paid for all of it and that too with foreign money.”

Foreigners have invested $6.3 billion in Indian equities this year compared with $9.9 billion in the first six months of 2014. Overseas fund managers bought stocks and bonds worth an unprecedented $42 billion last year, data compiled by Bloomberg show.

Growth Plans

The fund, which is currently managed by a five-member team that includes three analysts and a dealer, is branching out into private equity and plans to invest in sectors such as food processing, information technology and engineering-related startups.

Infina is setting up a subsidiary in Dubai to invest in overseas markets, especially in U.S. equities. The unit, in which Infina will initially invest 2 billion rupees ($31 million), is awaiting approval from the country’s central bank.

“My own comfort is more with investing in the U.S. market than in other overseas markets,” Subramanian said. “We will look at themes which we can’t get in other parts of the world. For instance in technology and biotech, where the U.S. market has world-beating companies.”

Read more at:

http://economictimes.indiatimes.com/articleshow/48579269.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

Led by regional activity and declining prices of global crude, panic investors took the index down almost 1,000 points intra-day before some relief occurred in the second half. At one point, the KSE-100 touched 34,275 points.

However, at close on Friday, the index lost 699.8 points or 1.99% to end at 34,519.77.

http://tribune.com.pk/story/942521/market-watch-tracking-regional-peers-index-sheds-700-points/

The current account deficit of the country shrunk to negative $159 million in July, the first month of the current fiscal year compared to negative $820 million in the same period last year, according to the data of State Bank of Pakistan (SBP) released on Thursday.

However, the country’s Gross Domestic Product (GDP) has gone up by $2.013 billion to $25.112 billion in July 2015 or current fiscal year, which is around 8.7 percent higher compared to $23.099 billion in July 2014. The current account percent of GDP is still in negative 0.6 percent compared to negative 3.5 percent in July 2014, the SBP data said..

However, the SBP report said that the current account was surplus to $730 million in January-March this year, but it started sliding to negative $534 in April-June 2015.

If compared on month-on-month basis, this deficit was stood at $820 million in July 2014, but the inflows from International Monetary Fund (IMF) and US Support Funds supported the current account of Pakistan in first month of the current fiscal year.

In the first month, the trade balance has also come down to negative $1.794 billion, shrinking by 37 percent compared to last year July figures of negative $2,112 billion. The export of the country remained at $1.760 billion while imports stood at $3.554 billion.

Services exports of the country enhanced to $681 million in the first month, while services imports declined to $591 million, which were stood at $351 million and $734 million in July 2014 respectively, the data said.

In July 2015, the country received an amount of $1.664 billion in the head of remittances, which was stood at $1.659 billion in the same period last year.

The country’s reserves stood at $18.655 billion this week, in which SBP’ reserves stood at $13.615 billion, while banks (other than SBP) reserves are at $5.039 billion.

After a meeting with Pakistani officials in Dubai this month — terrorism-prone Pakistan itself is considered too dangerous a venue — the IMF praised the Nawaz Sharif government’s “commitment and progress” in improving “economic resilience” and promoting growth and private sector jobs.

By some measures Pakistan is certainly recovering. Inflation and both the budget and current account deficits are down, while growth should reach 4.5 per cent in the current fiscal year. Foreign exchange reserves have increased to more than $13bn, covering three months of imports.

Pakistan’s private investors and independent economists, however, are not as sanguine as the IMF about the performance of a country that has long been a laggard in Asia and is struggling to create the millions of jobs a year it needs to employ newcomers to the workforce.

They argue that Islamabad has failed to use the financial windfall from lower oil prices to accelerate reform, has juggled the numbers for the IMF’s benefit to make some data look better than they really are, and has caused severe damage to the real economy with a perverse campaign to maintain a strong currency.

“We’ve been here before,” says Sakib Sherani of Macro Economic Insights, referring to the tenure of the military dictator Pervez Musharraf a decade ago when there was talk of Pakistan having turned the economic corner. The IMF and other cheerleaders, he says, “are all talking about something that’s quite different from the real economy: our ability to repay bondholders”.

The rise in reserves, Mr Sherani argues, is a “bit like a Ponzi scheme”, because most of the new reserves are borrowed from the IMF and other creditors.

As for the reduction of the fiscal deficit, it is based on harassing existing taxpayers more than on an overdue expansion of the tax base or a review of expenditure. “It’s only when you scratch the surface and look below that you find things are not really that great,” he says.

Mian Mansha, the Lahore-based tycoon reputed to be Pakistan’s richest man, is equally sceptical about the government’s record on reforming lossmaking state companies and the tax system. “There are only 350,000 people who pay more than $100,000 in tax, and five of them are in my house,” he says.

But Mr Mansha’s biggest gripe is about the impact of the strong Pakistani rupee — Ishaq Dar, finance minister, has kept it at about 100 to the dollar despite the US currency’s global strength — on his textile factories and other manufacturing plants.

“We are having a very tough time here in certain industries,” he says, noting that other garment exporters such as Turkey have stayed competitive following a sharp devaluation of their currencies.

Ashraf Wathra, central bank governor, insists previous devaluations have not helped exports. “There is no correlation at all,” he says. He defends Pakistan’s implementation of the latest IMF programme that ends in 2016 and describes the overall direction as “rather optimistic”.

Mr Sharif’s cabinet is also upbeat. Ahsan Iqbal, planning minister, says the current government is turning round the “disastrous situation” it inherited in 2013, and he sets great store by the infrastructure investment now promised by China.

“A country that people looked at as a safe haven for terrorists, they are now looking at as a safe haven for $46bn of Chinese investment,” he says. “We see Pakistan as a hub of trade and commerce in the region — south Asia, China and central Asia.”

The critics are not convinced, either by the future Chinese power stations — which they say look overpriced according to the limited project information available — or by the official economic data welcomed by the IMF.

http://www.ft.com/intl/cms/s/0/67422228-4594-11e5-af2f-4d6e0e5eda22.html#axzz3jeLFCfgp

The Motorway M-4 is a key part of the north-south transport corridor. Its area of influence, which includes Faisalabad, Multan, and the entire Punjab Province, accounts for approximately 56 percent of the country's population and 59% of the country's GDP. The M-4 motorway will extend the already completed M-1, M-2, and M-3 motorways southward and shorten the distance between Multan and the twin cities of Islamabad and Rawalpindi in the north. The Faisalabad to Gojra section (58km) of M-4 was completed in 2014 under ADB financing and the Khanewal to Multan section (57 km) will be completed in 2015 under financing from the Islamic Development Bank.

The project will finance the construction of the 62km Gojra Shorkot section, followed by the construction in 2016 of the remaining 64km Shorkot Khanewal section. The new motorway will provide a 4-lane access controlled alternative to the existing narrow and congested routes. This will be essential in providing relief for the heavily trafficked Faisalabad and Khanewal Multan Muzaffargarh areas.

ADB report revealed that the national highway N-5 is part of the north south transport corridor and Pakistan's longest and most important highway. Its section between Lahore and Multan is a 4-lane road that passes through highly urbanized areas carrying an average daily traffic volume of 20,000 vehicles. The completed M-4 will alleviate traffic congestion along the parallel N-5, and offer an efficient international link between the north of Pakistan and beyond, and southern Punjab, Sindh, and the ports of Karachi and Gwadar in southern Pakistan.

http://www.brecorder.com/money-a-banking/198/1221024/

The China-Pakistan Economic Corridor (CPEC), first proposed in 2013, is a massive project of rail links, special economic zones, dry ports and other infrastructure projects across Pakistan allowing for direct access to the Indian Ocean. It would connect Gwadar to Kashgar, a major trading hub in China, and abbreviate the current route to the Persian Gulf by more than 10,000 kilometers. Instead of 45 days, it would take China a mere 10 days to get its imports—all while avoiding any potentially contested channels near Taiwan, Vietnam, the Philippines, Indonesia and India, and eventually lowering shipping costs.

The CPEC would also provide China with an entry point to the Arabian Gulf, thus widening its geopolitical influence and possibly its military presence in the region. (Some Indian intellectuals suspect the Gwadar port will serve as a Chinese naval facility.) And it only comes at a cost of about $40 billion.

This isn’t the only investment China has planned in Pakistan. In fact, the money going to the country is double what Pakistan has received in foreign direct investment since 2008, and larger than any shape of assistance from the U.S. The list below (including CPEC) is just a snapshot of upcoming projects, likely funded by the Bank of China, the Export-Import Bank of China and the proposed Asian Infrastructure Development Bank:

$3.7 billion for a Karachi-Lahore-Peshawar rail line

$2.8 billion for developing four coal-fired stations with a capacity of 1,980 megawatts in Thar (Sindh)

$2.2 billion for two coal-mining blocks in Thar (Sindh)

$2 billion to build a natural gas pipeline between Gwadar and Nawabshah, then connecting to Iran

$2 billion to develop coal-fired generation plants at Port Qasim Karachi

$1.6 billion for a hydropower project in Karot

$1.2 billion for a solar power park in Bahawalpur

$930 million to link the Karakoram highway to Islamabad and Havelien

$260 million for a 100 megawatt wind farm in Jhimpir

$230 million to build the Gwadar International Airport

It is all part of China’s quest for influence throughout the continent via aid and investment. After decades of shying away from aggressive foreign policy moves, China now wants to play a much bigger regional role and is pushing plans for interconnected infrastructure networks to better link its economy with rest of Asia, the Middle East, Africa and Europe. Think of it as the new Silk Road.

http://www.forbes.com/sites/realspin/2015/08/25/china-looks-to-pakistan-to-expand-its-influence-in-asia/

Excerpts of Franklin-Templeton's Mark Mobius blog post titled "Building Corridors to the Future in Pakistan" dated Aug 24, 2015

Pakistan is an example of a country many investors have shunned due to negative news and perceptions, but our take is that often things aren’t always as sensational as may be reported. We do know that we have found some well-run companies in which to invest. We also believe that Pakistan will attract wider investor interest in the coming years for a number of reasons.

-------

China and Pakistan recently signed trade, energy and infrastructure agreements worth US$28 billion as part of a US$46 billion plan toward establishing the China-Pakistan Economic Corridor (CPEC), a combination of cooperative initiatives and projects that include connectivity, information network infrastructure, energy, industries and industrial parks, agricultural development and poverty alleviation, tourism and financial cooperation

----------

We have been investing in Pakistan for a number of years, and see it as an overlooked investment destination with attractive valuations due to negative macro sentiment. Pakistan has benefited from an improving growth outlook, continued efforts toward fiscal consolidation, steady progress in achieving structural reforms under the International Monetary Fund (IMF) program and ongoing support from regional partners.

------------

The Pakistani stock market has been one of the top-performing markets in the last five years (ended June 2015).3 The MSCI Pakistan Index has more than doubled with a 129% return during that time frame, compared with a 45% return for the MSCI Frontier Index and 22% increase in the MSCI Emerging Markets Index in US dollar terms.4 In our view, despite that strong performance, valuations of Pakistani stocks still remain relatively attractive. As of end-June 2015, the trailing price-to-earnings ratio of the MSCI Pakistan Index was 10 times, versus 11 times for the MSCI Frontier Index and 14 times for the MSCI Emerging Markets Index.5

The country’s macroeconomic environment has been improving in recent years. In recent months, easing inflation has allowed Pakistan’s central bank to cut its benchmark interest rate to its lowest level in 42 years. The IMF currently forecasts gross domestic product growth in Pakistan of 4.3% this year and 4.7% in 2016, up from 2.6% in 2010.6 The fiscal situation has also been improving, supported by multilateral disbursements in recent years as well as a recent international Sukuk issuance.7 More recently, lower oil prices have also improved the country’s trade balance, although exports have been impacted by lower cotton prices and a stronger rupee.

Elsewhere, we believe government efforts on expenditure control and divestments have been positive, but the government will need to remain committed to the economic and structural reform program. For foreign investors, the most important concerns are security and political stability. An internal anti-terrorism drive was made in the wake of the tragic Peshawar incident in December 2014, which targeted schoolchildren. We think these efforts need to be maintained over the longer term to develop a better security climate for businesses and the society as a whole. In the political environment, delays in the implementation of reforms or deterioration in the political or security situation could adversely impact the country’s macroeconomic development and fiscal position, hinder investment and weaken investor confidence.

....We think it’s an ideal time for Pakistan to implement reforms that will put electric power supply on a sound financial footing, enabling adequate supply at a reasonable price for local businesses that need to be internationally competitive.

Despite a number of ongoing challenges, we see many reasons for a brighter future for Pakistan.

SO LONG “taper tantrum”, hello “hike hysteria”. As the Federal Reserve has inched its way toward the first rise in its benchmark interest rate since 2006, emerging markets have felt the squeeze. China's stockmarkets have gyrated and plunged prompting a barrage of panicked interventions by the government. The Russian and Brazilian economies are expected to shrink this year, and emerging-market currencies are tumbling around the world. Some worry that the emerging world might be at risk of a repeat of the financial crises of 1997-8, when capital outflows wreaked havoc. To assess countries' vulnerability to a "sudden stop" in capital flows, The Economist has updated its capital-freeze index.

Our index focuses on three measures judged by economists to be serious risk factors: the current-account balance; private-sector credit growth; and the ratio of foreign debt to reserves. Each data point is indexed from 0 to 100 to make them comparable. A current account deficit of 10% or more of GDP corresponds to maximum vulnerability, while a surplus of 10% or higher corresponds to minimum vulnerability. A ratio of debt to reserves of 300% or more gets a value of 100, while a ratio of zero is set to zero. And average annual credit growth of 15% or more over three years receives a value of 100, while growth of 0% or less is set to 0. We have calculated the index for 2012 and for 2014, where the maximum risk of 300 is equivalent to the highest possible score across the three measures.

There are few surprises at the top of our list, where basketcases like Venezuela and Ukraine sit alongside troubled but less chaotic emerging markets like Turkey and Indonesia. Large oil producers have crept up the list. In 2012 Algeria ran a current-account surplus of more than 5%. Two years later, as oil prices plummeted, it had swung to a deficit of more than 4% of GDP (which is expected grow to 15% this year). Despite this, most large oil exporters remain relatively well positioned to withstand a capital-flow reversal thanks to large reserve surpluses; Russia's reserve hoard has meant the difference between a nasty recession and all-out financial collapse. On the other hand, Venezuela owes four times more than it holds in reserves, leaving it with no cushion against a financial drought.

Many emerging markets have reached for credit to prop up their economies amid slowing trade. In Turkey, credit growth has run at double-digit rates for most of the last six years. Credit is playing an increasing role in China's economy as well, where average growth in private borrowing rose to nearly 5% per year in the three years to 2014. Yet its mammoth reserve pile and trade position mean it remains near the bottom of the overall vulnerability measure, recent wobbles notwithstanding.

The three factors in our index are not the only ones that matter. Financial openness does too; China can rely on the additional protection of capital controls, which prevent investors from fleeing en masse (though those same controls are an obstacle to faster economic growth). Yet controls are never perfect. In recent months China has sold some reserves to provide support to its currency, which has nonetheless been dragged down by the change in global financial conditions. When the Fed begins hiking rates (as it will eventually, even if it declines to do so at its rate-setting meeting on September 16-17th) the pressure on fragile emerging markets will intensify. The swingeing drops in emerging-market currencies that have occurred so far may be a sign of more trouble to come.

With the earnings season about to start, the chart illustrates why the fate of the Indian markets depends on the ability of Q4 earnings to beat expectations.

As the chart shows, the Indian market is one of the most expensive in the world, immediately after the US, according to estimates from Citi Research.

At the current forward price-earnings multiple, the valuation for the Indian market is well above its mean.

To be sure, abundant liquidity, both from foreign and domestic investors, has been driving up stocks.

As the outlook for investment in real estate and gold has faded, investors have switched to equities.

But the record shows that markets fell in 2010, 2015 and 2016 from levels only slightly above current valuations. It’s time for earnings to catch up and for investors to be cautious.

http://www.livemint.com/Money/0fhFFLhZaqt3Gzm9ZMWOxH/India-is-one-of-worlds-most-expensive-stock-markets.html