Animal Droppings Help Catapult India's GDP Growth Rate Ahead of China's

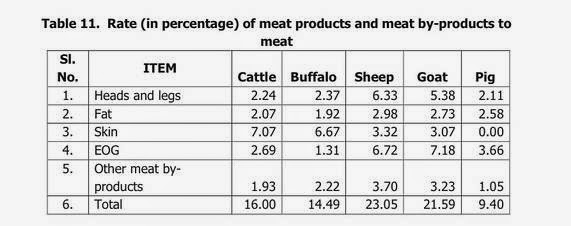

"The estimated “evacuation (defecation) rates” are 0.3 kilograms per day for goats and 0.8 kilograms per day for sheep. The study, titled “Positive Environmental Externalities of Livestock in Mixed Farming Systems of India,” was conducted jointly by the Central Institute for Research on Goats, in Makhdoom, Uttar Pradesh, and the National Center for Agricultural Economics and Policy Research in New Delhi. With all those “droplets” added in, the value of India’s livestock sector in the new GDP series is 9.1 billion rupees, or $150 million, higher than it was in the old series." Wall Street Journal on India's GDP RevisionsAnimal droppings (BS) is just one of many innovations of Central Statistical Office (CSO) that are being used to support India's claim to be growing faster than China. Until early February, when CSO changed the way it measures economic activity, India was enduring its weakest run of growth since the mid-1980s. Now it is outpacing China, having grown an annual 7.5% in the fourth quarter of last year, reports Business Standard.

|

| Indian Livestock GDP Calculations. EOG=Edible Offals, Glands. Source: CSO Via WSJ |

While India's boosters in the West are not only buying but applauding the new figures, Indian policy professionals at the nation's Central Bank and the Finance ministry are having a very hard time believing the new and improved GDP brought to the world by Indian government. Dissenters include Morgan Stanley's Ruchir Sharma, an Indian-American, who has called the new numbers a "bad joke" aimed at a "wholesale rewriting of history".

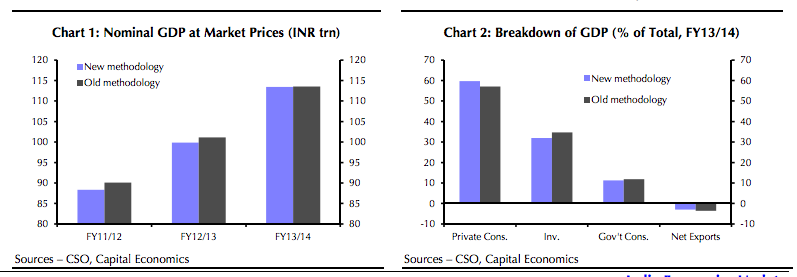

Based on the latest methodology, it is claimed that the Indian economy expanded 7.5 percent year-on-year during the last quarter, higher than 7.3 percent growth recorded by China in the latest quarter, making it the fastest growing major economy in the world, according to Reuters. Is it wishful thinking to make Indian economy look better than China's?

|

| India GDP Revisions. Source: Financial Times |

The GDP revisions have surprised most of the nation's economists and raised serious questions about the credibility of government figures released after rebasing the GDP calculations to year 2011-12 from 2004-5. So what is wrong with these figures? Let's try and answer the following questions:

1. How is it possible that the accelerated GDP growth in 2013-14 occurred while the Indian central bankers were significantly jacking up interest rates by several percentage points and cutting money supply in the Indian economy?

2. Why are the revisions at odds with other important indicators such as lower industrial production and trade and tax collection figures? For the previous fiscal year, the government’s index of industrial production showed manufacturing activity slowing by 0.8%. Exports in December shrank 3.8% in dollar terms from a year earlier.

3. How can growth accelerate amid financial constraints depressing investment in India? Indian companies are burdened with debt and banks are reluctant to lend.

4. Why has the total GDP for 2013-14 shrunk by about Rs. 100 billion in spite of upward revision in economic growth rate? Why is India's GDP at $1.8 trillion, well short of the oft-repeated $2 trillion mark?

Questions about the veracity of India's economic data are not new. US GAO study has found that India's official figures on IT exports to the United States have been exaggerated by as much as 20 times.

Similarly, French economist Thomas Piketty has argued in his best seller "Capital in the Twenty-First Century that the GDP growth rates of India and China are exaggerated. Picketty writes as follows:

"Note, too, that the very high official growth figures for developing countries (especially India and China) over the past few decades are based almost exclusively on production statistics. If one tries to measure income growth by using household survey data, it is often quite difficult to identify the reported rates of macroeconomic growth: Indian and Chinese incomes are certainly increasing rapidly, but not as rapidly as one would infer from official growth statistics. This paradox-sometimes referred to as the "black hole" of growth-is obviously problematic. It may be due to the overestimation of the growth of output (there are many bureaucratic incentives for doing so), or perhaps the underestimation of income growth (household have their own flaws)), or most likely both. In particular, the missing income may be explained by the possibility that a disproportionate share of the growth in output has gone to the most highly remunerated individuals, whose incomes are not always captured in the tax data." "In the case of India, it is possible to estimate (using tax return data) that the increase in the upper centile's share of national income explains between one-quarter and one-third of the "black hole" of growth between 1990 and 2000. "

T.C.A. Anant, the chief statistician of India, has told the Wall Street Journal that “there’s a large number of areas where we have deviated (from the United Nations’ latest guidebook on measuring GDP) for a large measure, because we are simply, at the moment, unable to implement those recommendations.”

Related Links:

Haq's Musings

Is India Fudging GDP to Look Better Than China?

India's IT Exports Highly Exaggerated

India-Pakistan Economic Comparison 2014

Pakistan's Official GDP Figures Ignore Fast Growing Sectors

Challenging Haqqani's Op Ed: "Pakistan's Elusive Quest For Parity"

State Bank Says Pakistan's Official GDP Under-estimated

Pakistan's Growing Middle Class

Pakistan's GDP Grossly Under-estimated; Shares Highly Undervalued

Fast Moving Consumer Goods Sector in Pakistan

3G-4G Roll-out in Pakistan

Comments

The new and not-so-funny numbers show that the Indian economy grew at a pace of 6.9% in the last fiscal year, a claim that is fantastic in the extreme. Many Indian economists have set out to show that the new growth numbers for the economy as a whole simply don’t add up, as a sum of the parts. Every piece of data — from the tepid increase in corporate revenues to imports, credit, rail freight and auto sales — points to a much lower growth figure, probably closer to the old estimate of 5%.

Surprisingly, for a country obsessed with its GDP growth rate, there is not much outrage at this travesty, either in public or at cocktail parties. In the past, India’s habit of revising economic data was confined to relatively minor tweaks, but this latest update is a wholesale rewriting of history. In the international financial community, no one had questioned the veracity of India’s economic numbers, until now.

This makes India look bad even compared to China, which many analysts have long suspected of massaging GDP figures to show steady growth. But the same sceptical analysts admit that when China manipulates its numbers, it does so carefully and only when the actual growth rate falls below its official target, as it has of late. The authorities seem to know exactly what they are doing. India’s new GDP data clashes even with the pronouncements of some government and central bank officials, suggesting that the left arm doesn’t seem to know what the right arm is doing.

The whole episode is reinforcing the bad rap India gets for poor governance standards. To be sure, many emerging nations including Turkey and Nigeria have issued flattering upward revisions of their growth data in recent years, but generally without eliciting peals of laughter. Last year, Nigeria issued a revision showing that the economy was nearly twice as large as previously reported, but it was widely accepted because the new methodology was well explained and had the endorsement of the International Monetary Fund.

The IMF in fact recommends that, every five years, countries update the base year they use to calculate the pace of growth in the economy. The idea is to capture the impact of new growing industries, and Nigeria hadn’t updated its base year since 1990. India’s last revision came in 2010, so this one came on schedule. Only the statistics bureau clearly rushed it into print, without conducting even an elementary ‘smell test’ to ensure that the new numbers square with the reality on ground. One clear sign of the bureau’s haste to publish is the fact that it released revised data for only the last two years, making it impossible to see the long-term trend for India’s growth rate.

Nobody really believes that the Indian economy grew at anywhere close to 7% last year, and shockingly no one is willing to put an end to this nonsense. When India delivers its budget on February 28, officials are likely to claim that economic growth in the coming year will accelerate to around 8% — a figure based on the new series. A forecast based on dodgy numbers will only cast doubt on India’s claim to be the world’s fastest-growing large emerging market, though that claim could easily prove true in a couple of years, based on credible numbers.

http://blogs.timesofindia.indiatimes.com/toi-edit-page/6-9-growth-world-laughing-at-this-bad-joke/

Indian economy would collapse without such inflows.

Read the following to get a sense of the magnitude of foreign capital inflows in India:

"Strong capital flows to India in the recent period reflect the sustained momentum in domestic

economic activity, better corporate performance, the positive investment climate, the longterm

view of India as an investment destination, and favourable liquidity conditions and

interest rates in the global market. Apart from this, the prevailing higher domestic interest

rate along with a higher and stable growth rate have created a lower risk perception, which

has attracted higher capital inflows.

The large excess of capital flows over and above those required to finance the current

account deficit (which is currently around 1.5% of GDP) resulted in reserve accretion of

$110.5 billion during 2007/08. India’s total foreign exchange reserves were $308.4 billion as

of 4 July 2008."

http://www.bis.org/publ/bppdf/bispap44m.pdf

"Gross capital flows have increased nearly 22 times from $42.7 billion in 1991-92 to over $932.3 billion in 2010-11. As a

share of GDP, this amounted to an increase from 15.5% in 1991-92 to 55.2% in 2010-11. Much

of the increase in financial integration occurred between 2003-04 and 2007-08. Given the

impressive economic performance indicated by close to 9% growth rate, higher domestic

interest rates and a strong currency, India's risk perception was quite low during 2003 to 2007.

Furthermore, this period was associated with favorable global conditions in the form of ample

liquidity and low interest rates in the global markets—the so-called period of Great Moderation."

http://www.adb.org/sites/default/files/publication/30234/management-capital-flows-india.pdf

Interestingly, even as some investors are getting edgy and expect quick government action on various fronts, observations from some of the international institutions that came in this month were largely optimistic about the future of the Indian economy. Encouraged by the recent policy action, rating agency Moody’s, while affirming its Baa3 rating on India, changed its outlook to positive from stable. It said in a statement: “…recent measures to address inflation, keep external balances in check, simplify the regulatory regime for investors, increase foreign direct investment, and facilitate infrastructure development will reduce some of India’s sovereign credit constraints.”

The government’s intent to improve the economic environment and action taken in this regard is being recognized. “Growth will benefit from recent policy reforms, a consequent pick-up in investment, and lower oil prices. Lower oil prices will raise real disposable incomes, particularly among poorer households, and help drive down inflation,” said the latest World Economic Outlook (April 2015) of the International Monetary Fund (IMF). Growth in India, according to the IMF, will be higher than that in China in 2015 and 2016, making it the fastest growing large economy in the world. It expects India to grow at 7.5% in both 2015 and 2016. Meanwhile, the Chinese economy is expected to expand at an annual pace of 6.8% and 6.3%, respectively.

The World Bank had similar observations about the Indian economy. In its South Asia Economic Focus (Spring 2015) report, it noted, “India’s economy is poised to accelerate on the back of an ambitious reform agenda, and faster growth is expected to further drive down poverty.” The acceleration in growth, according to the World Bank, will be led by investment, which is expected to grow at an average rate of 12% between 2015 and 2017.

However, not all are equally enthused. A recent report (India’s Fiscal Roadblocks Could Stall Infrastructure Progress) by Standard & Poor’s presented a different picture. “India’s public finances are less than rock solid due to long-standing cracks in its budgetary system. While the country’s budgetary performances have strengthened in recent years, its hard-won fiscal improvements could yet unwind because of a financial or commodity shock,” the report said. It also highlighted that further reforms will be required on the fiscal front to be able to sustain higher investment spending. Efficient subsidy spending, which can free up resources for capital spending, is necessary to attain and maintain higher growth in the medium to long term. Both markets and policymakers will do well by paying attention to Standard & Poor’s observations. In fact, a financial or commodity shock can not only affect the progress made on the fiscal front, but also the wider economy.

http://www.livemint.com/Money/jClwqMpuzmMK1Dksx3iLQL/How-the-world-is-viewing-India-and-some-emerging-challenges.html

Is PM Narendra Modi running out of luck? He had famously boasted being a lucky Prime Minister while seeking votes during the Delhi elections. The context, of course, was international oil prices had less than halved and that seemed to have brought all round uptick in economic sentiment, what with the stock markets soaring to new highs early 2015. Consensus among global FIIs was that they will remain overweight India as compared to other markets like China, Brazil, South Korea, Taiwan and Russia. But everything seems to be reversing over the past month and a half.

Suddenly the FIIs, with a cumulative investment in Indian stocks of about $300 billion at market value, are looking at other emerging stock markets for returns and no longer treat India as the most preferred destination as they did last year, and even the beginning of this year. FII net outflows gave been of the order of Rs 12,500 crore over the past month. The stock market index has seen the biggest correction of 10 percent in a short time. This has caused speculation whether the markets are slipping into a bear phase.

But what is indeed worrisome is India is probably the worst performing stock market among emerging economies this year. This is in sharp contrast to the view taken by the big FIIs that the Modi government reforms could trigger a multi-year bull run in India. Now the same FIIs are shifting the weightage of their global allocation to China where the stock markets have shown 30 percent growth since January. India's Sensex growth remains in negative territory. Even FII inflows, which primarily influence market movement, are flat to negative since January.

Worse, now FIIs also seem to prefer oil exporting markets like Russia and Brazil, both of whom had fallen out of favour after the global oil prices had more than halved, badly affecting their revenues. Now the FIIs believe that oil prices are moderately correcting and returning to oil exporting markets like Russia and Brazil makes sense. This view is buttressed by another major consideration. They feel as the US economy recovers and the prospect of monetary tightening by the Federal Reserve brightens, the dollar would strengthen in the short to medium term.

The Economic Times has just reported a survey of top CEOs and the majority of them suggest that demand is depressed. "The bonhomie and cheer that greeted the arrival of the Modi government is replaced by a sombre mood and a grim acknowledgement of the realities of doing business in India," reports ET, as it captures the sentiment of the CEOs. Little wonder that this is reflecting in the behaviour of the stock market and currency. The largest engineering conglomerate L&T had said some of its plants are lying idle as demand for capital goods is very weak. The Aditya Birla Group had deferred its revenue target of $65 billion by 3 years, to 2018.

These are not good signs for the economy and both the stock market and currency will reflect this in the months ahead.

http://www.firstpost.com/business/worst-performing-stock-market-end-modi-bubble-fiis-2243556.html

Months after the release of the new GDP methodology with much higher numbers, it still remains wildly inconsistent with numerous other indicators, pointing to continued economic slack.

The revised GDP numbers particularly pose dangers for monetary policy decisions, as much of India expects the RBI to cut rates.

RBI Governor Raghuram Rajan and the government’s Chief Economic Adviser Arvind Subramanian, two trained economists, remain 'puzzled' with the new numbers.

Part I of this article series looked at the change in the methodology of calculating India's GDP that literally overnight transformed an 'ailing' economy into one of the best performing economies globally. The problem is not with the methodology per se. The methodology is the same that is globally accepted; the problem is with the missing comparable numbers as per the older methodology, and the missing longer term historical data for the new one (not necessary that historical data beyond three years be made public, but it should at least be made available to statisticians doing the exercise and to other approved authorities for scrutiny/confidence building).

-------

Presented here are some of the related data over the years to get a comprehensive picture. The Index of Industrial Production (IIP) data reveal two insights: Post 2008, there may have not been a sustainable recovery but a sharp bounce back in 2011 which can be attributed to a typical inventory bounce back as normally seen after a period of sharp decline like the one during the 2008-09 period. In a slowdown, cut back in production is multiplied by the effect of sharp inventory reductions, making the situation even worse. An inventory bounce back is the opposite of it. With signs of recovery, companies start filling up shelves again faster than the real demand. The Economist blog, referred in Part I, first suggested that based on the IMF's World Economic Data following market prices, India grew faster than China in the April-March 2010-11 financial year of India's vis-à-vis China's calendar year of 2010. This observation synchronizes well with the inventory bounce back of IIP numbers observed in the following IIP chart.

The IIP for March, reported on 12th May, came in at a five-month low of 2.1%, making the yearly average for 2014-15 at 2.8% compared to a contraction of 0.1% for 2013-14.

True, there are masquerading voices within India with political inclinations who find nothing wrong in this overnight cure of the ailing economy. The same voices blamed the last government for the economic slowdown, which now becomes imaginary, as per the new methodology. The falling earnings (the last quarterly earnings of 101 companies, that declared results by 27th April or so, fell by 9.23%) and the continuous deterioration of balance sheets of companies, especially banks, convincingly debunk any such hypothesis. It also exposes the charade behind the new GDP numbers. Merely stating how the IIP numbers simply do not matter anymore in the methodology, directly or indirectly, may not be the whole truth. The deterioration of balance sheets is the root cause for the increasing NPAs in Indian banks, mostly state-owned ones, without any certainty as of now on whether or not NPAs have reached a saturation level. This is what RBI Governor Rajan said on NPAs on 17th April:

"The non-performing assets have been growing. I'm hopeful that we are near the peak or that we have even passed the peak, but we won't know until it is truly clear with the passage of time."

Similarly, a look at India's trade data shows a sharper slowdown (21%) in exports than in imports (13%) for the last reported month (March 2015). There is an overall decline in both for the year too.

http://seekingalpha.com/article/3180526-myth-or-reality-scrutinizing-indias-revised-gdp-numbers-and-secular-bull-market-part-ii

http://www.livemint.com/Politics/DQcWH6FIUXGnhDpFfLbmFP/Indias-exports-contract-202-in-May-their-sixth-monthly-f.html …

The Indian commerce ministry announced on Tuesday that India’s exports fell 20.2 percent compared with the same month last year (LiveMint, Reuters). This announcement makes May the sixth consecutive month in which exports have fallen and this is the the longest such streak since 2009. The ministry also announced that imports fell by 16.5 percent, bringing the overall trade deficit to a 3 month low. According to the data gathered by Bloomberg, in May, oil imports fell 41 percent to $8.53 billion, non-oil imports fell 2.2 percent to $24.21 billion however gold imports grew 10.5 percent to $2.42 billion. A weakening rupee and an acceleration in inflation indicates maneuverability is decreasing for Reserve Bank of India (RBI) governor Raghuram Rajan to lower interest rates any further. RBI has already cut the interest rates in the country three times this year.

The Indian rupee touched the day’s low soon after the data. The currency has weakened 2.1% over the past three months, the fourth-worst performance among 24 emerging market currencies tracked by Bloomberg. Bloomberg

http://www.livemint.com/Politics/DQcWH6FIUXGnhDpFfLbmFP/Indias-exports-contract-202-in-May-their-sixth-monthly-f.html

India registered 7% growth between April and June on Monday, making it one of the world’s fastest-growing economies, according to official data.

But other key indicators of economic vitality aren’t as positive.

Vehicle sales last quarter didn’t show the kind of growth you would expect from an economy expanding at a rate of more than 7% per year. Car, truck and two-wheeler sales are good indicators of consumers, corporate and farmer sentiment respectively. Overall vehicles sales barely budged last quarter, rising just 1% to 4.89 million vehicles. Passenger vehicle sales were up 6.17%, commercial vehicle sales were up 3.55% and two-wheeler sales were up just 0.64%.

Indian officials had hoped for a pick-up in overseas demand for Indian-made products as Western economies gathered momentum. But the country’s exports have fallen for eight months in a row through July, underscoring continued stress in global economies.

In the year ended March 31, India’s exports totaled $310.5 billion, falling about 9% short of the $340 billion target. In the first four months of the current fiscal year things haven’t improved: goods exports have recorded a 15% decline–compared with the same period last year–to $89.83 billion. China’s move to devalue its currency has given its producers a competitive edge, damping export prospects of other economies, including India. In addition, the sharp drop in global crude oil prices, while good for India’s import bill, has come as a major downer for Indian petroleum product exports, which make up a big chunk of the South Asian economy’s total shipments.

The Indian currency hit a near two-year low against the dollar last week in the midst of the global selloff and was among the worst performing currencies in Asia. Fear among investors that the slowdown in China could cause a global slump was the main drag on the Indian currency. Analysts say the depreciation in the rupee is necessary to keep India’s exports competitive. They expect some more weakness later this year, depending on the U.S. Federal Reserve’s decision on lending rates. Foreign investors became big sellers in the Indian debt market in August, putting pressure on the rupee as they took dollars out of the local market.

The benchmark Sensex index was one of the top-performing indexes last year, but so far this year it has failed to shine. Since mid-2014, investors bought stocks on hopes that the economy would rise faster and boost profits. But that outcome has been elusive and analysts have started cutting their Sensex targets. Ambit Capital now sees the Sensex falling to 28,000 points, down from its earlier target of 32,000. If the Chinese devalue the yuan again, the Indian stock market could fall further.

Profits at big companies have barely budged since Prime Minister Narendra Modi came to power in India last year. The chart above shows the percentage growth of profits of companies in the benchmark Sensex index compared to a year earlier.

According to a Bank of America Merrill Lynch report, the profits of Sensex companies rose by only 1% during the April through June quarter, compared with 24% growth in the same period a year earlier.

Utilities and cement companies have dragged the average earnings growth as big private sector and government projects remained stuck waiting for government approvals. Metal and refining companies suffered due to the decline in oil and commodity prices.

http://blogs.wsj.com/indiarealtime/2015/09/01/5-indicators-that-contradict-indias-gdp-figures/

The slump in exports by 20.1% in August seems to have finally set alarm bells ringing as the exporters are now demanding that both the prime minister and commerce minister step in to help and prop up the sector. The demand is reasonable given that exports have now fallen for the ninth consecutive months dragging down total exports by 16.2% in April-August 2015-16. It is also worrisome because the fall in exports have now stretched into the second year having already fallen by a marginal 1.2% in 2014-15.

So far the government has tried to cover up the discordant trends on the trade front by pointing to the steady improvement in the current account deficit numbers which have now fallen to around 1.2% in the most recent quarter after peaking at above 5% just a few years back. However, the fall in current account deficit has little to do with export performance as it happened largely to the slump in oil prices and the restraints placed on gold imports.

But now the scenario has deteriorated far below acceptable levels. Exports as a percentage of the GDP has fallen from a high of 16.8% of the GDP in 2011-12 to 15.4% in 2014-15. The fall in goods exports has substantial repercussion not only on growth of the economy and also on the NDA governments much vaunted Make in India programme. Studies have pointed out that few countries have been able to grow at 7% plus growth rates based on domestic demand alone.

Numbers for the first five months of the year show that the fall in exports have been across board. Asia, which is India’s largest export market accounting for almost half the total exports, has been badly effected with exports declining by 16.2%. The scenario was no different in the EU, our second largest export market that accounts for close to a fifth of our imports, which also saw exports decline by 10.5%. Worse effected was West Asia our third largest market where exports fell by 16%. Markets in Asean also registered a fall of 22.7%. The only consolation was the exports to USA, which accounts for 16% of our total exports, registered a minimal fall of 1.1%.

http://blogs.timesofindia.indiatimes.com/crowdsourced/falling-exports-will-derail-the-make-in-india-efforts-and-slowdown-gdp-growth-rates/

The skepticism arrived soon after India’s Central Statistical Office (CSO) put out revised GDP numbers last January.

India’s chief economic advisor, Arvind Subramanian, said he was puzzled and mystified by the revised estimates based on a new methodology, which instantly raised the country’s GDP growth from 4.7% to 6.9% for the 2013-14 fiscal year. Ruchir Sharma, head of emerging markets and global macro at Morgan Stanley Investment Management, called it a “bad joke.” And Raghuram Rajan, the governor of the Reserve Bank of India (RBI), said he didn’t want to talk about it until he understood the numbers better.

A whole year later, institutions like the RBI are so befuddled—and seemingly unconvinced—by India’s revised GDP numbers that they are looking at a range of other indicators to understand the true state of Asia’s third-largest economy.

“Like other economists, the RBI is now turning to hybrid models that mix elements of the old and new GDP methods to get a better feel for the underlying health of the economy,” Reuters reported on Feb. 5.

In particular, India’s central bank is tracking two-wheeler sales, car sales, rail freight, and consumer goods sales in rural areas “to get a better understanding of the ground realities,” an RBI official told Reuters. Quartz has emailed the RBI for comment, and will update if the bank replies.

The key contradiction is that even as prime minister Narendra Modi makes public declarations of India’s newfound status as the world’s fastest-growing major economy, key sectors such as manufacturing and agriculture are still stuck in a rut.

“The economy is recovering but it’s hard to be very definitive about the strength and breadth of the recovery for two reasons—economy is sending mixed signal and second there is some uncertainty how to interpret GDP data,” Subramanian explained late last year.

Economists and investors are increasingly showing that they have little or no confidence in India’s official economic data – presenting whoever is elected as the next prime minister with an immediate problem.

There have been questions for many years about whether Indian government statistics were telling the full story but two recent controversies over revisions and delays of crucial numbers have taken those concerns to new heights.

The government itself has admitted there are deficiencies in its data collection.

A study conducted by a division of the statistics ministry in the 12 months ending June 2017 found that as much as 36 percent of the companies in the database used in India’s GDP calculations could not be traced or were wrongly classified.

But the ministry said there was no impact on GDP estimates as due care was taken to adjust corporate filings at the aggregate level.

Last December, the government held back the release of jobs data but an official report leaked to an Indian newspaper showed the unemployment rate had touched its highest level in 45 years.

Economists and investors are now voting with their feet – by using alternative sources of data and in some cases creating their own benchmarks to measure the Indian economy.

Ten economists and analysts at banks, think-tanks and foreign funds interviewed by Reuters said they were moving to use alternative data sources, or at least official data of a different kind.

Among the numbers they prefer are fast-moving indicators like car sales, air and rail cargo levels, purchasing managers’ index data, and proprietary indices created by the institutions themselves to track the economy.

Many economists said they were stunned when the government upwardly revised GDP growth for 2016/17 to 8.2 percent from 6.7 percent, although the demonetization of high value notes hit businesses and jobs in that financial year.

“Our response has been to spend time developing an Indian Activity Index, which takes a range of time series data that in the past were strongly correlated with real GDP growth and extract the common signal from them,” said Jeremy Lawson, chief economist at Aberdeen Standard Investments, which manages more than $700 billion in assets.

The preliminary evidence from the index, which includes components like car sales, air cargo and purchasing managers’ index data suggests the government has over-estimated GDP growth, he said.

“Our index would suggest that there was stable growth, rather than the rapid acceleration suggested by the GDP figures,” he said, referring to three years of data from 2014.

Even those close to the government have said the lack of accuracy in the official data makes it much more likely that authorities will miss major swings in activity and be unable to react quickly to head off a crisis. It is also a problem for investors who may be misled into thinking the economy is more robust than it really is.