Economic History of South Asia Region Since 1 AD

When the British arrived in Mughal India, the country's share of the world GDP was 25%, about the same as the US share of the world GDP today. By 1947, undivided India's share of world GDP ($4 trillion in in 1990 Geary-Khamis dollars) had shrunk to about 6% (India: $216 billion, Pakistan: $24 billion). Since independence, India's contribution to world GDP has shrunk further to about 4%, according to British Economist Angus Maddison who died in 2010.

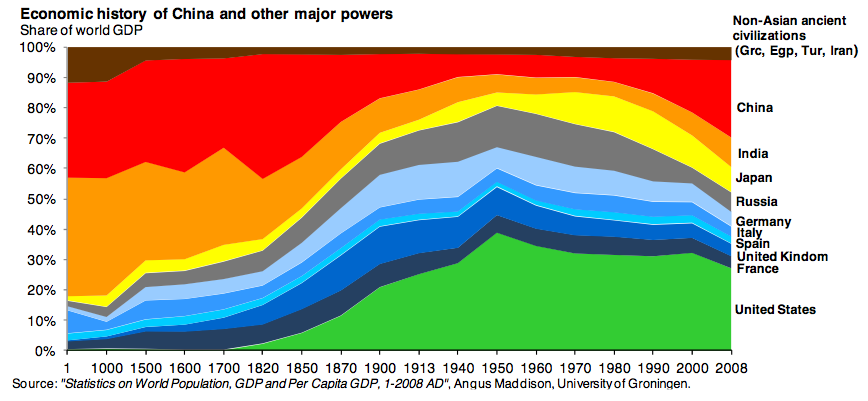

The colonization of India and many other nations in Asia and Africa began with the advent of the Industrial Revolution in Europe which resulted in a major power shift from East to West over the time-span of just a few decades. Prior to the Industrial Revolution, the world depended mainly on agriculture based on human and animal muscle power. Countries with large populations and farmlands had large share of the world GDP. The per capita productivity differences among nations and regions were relatively small. The machine age changed it all. Those who used machines became much more productive and significantly richer than the rest.

In 1000 AD, according to British Economist Angus Maddison, China and India together accounted for more than half of the world GDP (calculated in 1990 dollars in terms of purchasing power parity). By 1600, that share was 51.4%, with China accounting for 29% and India 22.4% of world GDP. A hundred years later, China’s GDP had fallen but India’s went up to 24.4% of world output. By 1820, however, India’s share had fallen to 16.1%. By 1870, it went down to 12.2%. International Monetary Fund (IMF) projections indicate that India’s share of world GDP would be 6.1% in 2015.

While it is a fact that India's total GDP was at one point the highest in the world, does it mean that the average Indian was richer than his or her counterparts elsewhere in the world? To answer this question, let's look at Maddison's figures for per capita GDP in various parts of the world.

While it is a fact that India's total GDP was at one point the highest in the world, does it mean that the average Indian was richer than his or her counterparts elsewhere in the world? To answer this question, let's look at Maddison's figures for per capita GDP in various parts of the world.

In 1 AD, India’s GDP per capita was $450, the same as China’s. But Italy under the Roman Empire had a per capita income of $809. In 1000 AD, India’s per capita income was $450 and China’s $466. But the average of the Islamic Caliphate in Baghdad which ruled West Asia (Turkey, Syria, Iran and Iraq) was much higher at $621. An average citizen of the Abbasid Caliphate was richer than an average Indian or Chinese. In fact, the per capita income in the Abbasid Caliphate was the highest in the world in 1000 AD.

As the European Renaissance began, new centers of prosperity emerged. Italy topped the table in 1500 AD, with per capita income of $1,100, the Netherlands following with a per capita income of $761. The UK was not far behind, with a per capita income of $714. All of these nations were richer than India and China which had per capita incomes of $550 and $600 respectively.

While India today has the world's largest population of poor, it is still richer than it has ever been in terms of per capita incomes. Indians are also living longer than ever in the country's history; average life expectancy in India has risen from just 23 years in 1800 to 65.5 years now. However, India continues to significantly lag the rest of the world on both economic and social indicators.

Related Links:

Haq's Musings

Power Shift Since Industrial Revolution

Can Superpoor India Become a Superpower?

India: World's Largest Population of Poor, Hungry and Illiterates

Sri Lanka Leads South Asia in Economic and Social Indicators

Upwardly Mobile Pakistan

Brief History of Pakistan Economy

India Ranks Last on PISA, TIMSS

The colonization of India and many other nations in Asia and Africa began with the advent of the Industrial Revolution in Europe which resulted in a major power shift from East to West over the time-span of just a few decades. Prior to the Industrial Revolution, the world depended mainly on agriculture based on human and animal muscle power. Countries with large populations and farmlands had large share of the world GDP. The per capita productivity differences among nations and regions were relatively small. The machine age changed it all. Those who used machines became much more productive and significantly richer than the rest.

In 1000 AD, according to British Economist Angus Maddison, China and India together accounted for more than half of the world GDP (calculated in 1990 dollars in terms of purchasing power parity). By 1600, that share was 51.4%, with China accounting for 29% and India 22.4% of world GDP. A hundred years later, China’s GDP had fallen but India’s went up to 24.4% of world output. By 1820, however, India’s share had fallen to 16.1%. By 1870, it went down to 12.2%. International Monetary Fund (IMF) projections indicate that India’s share of world GDP would be 6.1% in 2015.

In 1 AD, India’s GDP per capita was $450, the same as China’s. But Italy under the Roman Empire had a per capita income of $809. In 1000 AD, India’s per capita income was $450 and China’s $466. But the average of the Islamic Caliphate in Baghdad which ruled West Asia (Turkey, Syria, Iran and Iraq) was much higher at $621. An average citizen of the Abbasid Caliphate was richer than an average Indian or Chinese. In fact, the per capita income in the Abbasid Caliphate was the highest in the world in 1000 AD.

As the European Renaissance began, new centers of prosperity emerged. Italy topped the table in 1500 AD, with per capita income of $1,100, the Netherlands following with a per capita income of $761. The UK was not far behind, with a per capita income of $714. All of these nations were richer than India and China which had per capita incomes of $550 and $600 respectively.

|

| India Health-Wealth Indicators Source: Gapminder.com |

While India today has the world's largest population of poor, it is still richer than it has ever been in terms of per capita incomes. Indians are also living longer than ever in the country's history; average life expectancy in India has risen from just 23 years in 1800 to 65.5 years now. However, India continues to significantly lag the rest of the world on both economic and social indicators.

Related Links:

Haq's Musings

Power Shift Since Industrial Revolution

Can Superpoor India Become a Superpower?

India: World's Largest Population of Poor, Hungry and Illiterates

Sri Lanka Leads South Asia in Economic and Social Indicators

Upwardly Mobile Pakistan

Brief History of Pakistan Economy

India Ranks Last on PISA, TIMSS

Comments

The skepticism arrived soon after India’s Central Statistical Office (CSO) put out revised GDP numbers last January.

India’s chief economic advisor, Arvind Subramanian, said he was puzzled and mystified by the revised estimates based on a new methodology, which instantly raised the country’s GDP growth from 4.7% to 6.9% for the 2013-14 fiscal year. Ruchir Sharma, head of emerging markets and global macro at Morgan Stanley Investment Management, called it a “bad joke.” And Raghuram Rajan, the governor of the Reserve Bank of India (RBI), said he didn’t want to talk about it until he understood the numbers better.

A whole year later, institutions like the RBI are so befuddled—and seemingly unconvinced—by India’s revised GDP numbers that they are looking at a range of other indicators to understand the true state of Asia’s third-largest economy.

“Like other economists, the RBI is now turning to hybrid models that mix elements of the old and new GDP methods to get a better feel for the underlying health of the economy,” Reuters reported on Feb. 5.

In particular, India’s central bank is tracking two-wheeler sales, car sales, rail freight, and consumer goods sales in rural areas “to get a better understanding of the ground realities,” an RBI official told Reuters. Quartz has emailed the RBI for comment, and will update if the bank replies.

The key contradiction is that even as prime minister Narendra Modi makes public declarations of India’s newfound status as the world’s fastest-growing major economy, key sectors such as manufacturing and agriculture are still stuck in a rut.

“The economy is recovering but it’s hard to be very definitive about the strength and breadth of the recovery for two reasons—economy is sending mixed signal and second there is some uncertainty how to interpret GDP data,” Subramanian explained late last year.

Now Hindutva rulers are trying to erase Muslim history in India. They can not succeed.

Muslims have given the world algebra, calculus, scientific method, physics, astronomy, medicine, philosophy, social sciences and a whole lot more.

Watch Prof Roy Casagranda explain it in detail in the following video:

https://youtu.be/C8M4i9fvq1M

How India's Economy Will Overtake the U.S.'s

https://time.com/6297539/how-india-economy-will-surpass-us/

As for population size, India likely surpassed China this year to become the world’s most populous country, and the gap will only widen in the near future. That confers additional benefits through economies of scale in the provision of public goods. Take, for example, India’s digital payments infrastructure built on the biometric identity system known as Aadhaar and the United Payments Interface (UPI) platform, which serves as host to hundreds of banks. Using Aadhaar to verify identity, UPI clears transactions between bank-account holders in real-time. The larger the number of users, the lower the per-capita cost of building the infrastructure for it.

This same argument also applies to other sectors. Once an expressway has been built, for example, the larger the population in the communities residing around it, the lower the per-capita cost of connecting them to it. The same goes for railway and air connectivity, electricity, and piped water. Once these amenities have been brought to one village, the extra cost of extending them to other nearby villages is small.

Size also brings benefits when it comes to creating supply chains. A larger population means greater scope for agglomeration and cost efficiencies. Today, with the risks of investing and operating in China multiplying, multinationals are switching to the so-called "China+1" strategy, looking for an additional, less risky but cost-effective location for their investments. India has a distinct advantage in becoming that "+1" country because it constitutes the largest single market among potential competitors. Components produced in different locations can move freely without having to face a customs border. A large internal labor market also makes for better prospects for a closer match between the skills needed and those available.

But first, India needs to reduce its trade protectionism, which remains relatively high. No country has sustained growth rates of at least 8%, as India needs to do to overtake the U.S. economy, without embracing globalization. The country should roll back tariffs, strike more free trade deals with major economies and trade blocs, and cut back on the use of anti-dumping.

There are additional areas where India cannot afford to be complacent. The country must swiftly privatize a number of public sector enterprises, particularly banks, that have a long history of low or negative returns. Tax reform should also be high on the government's agenda; a constant complaint of businesses, especially small- and medium-sized ones, has been overzealous tax authorities and a convoluted and opaque system.

In essence, India needs to remember the spirit of its economic reforms in 1991—which centered around liberalization, privatization, and globalization—that have gone some distance toward accelerating growth. If the country wants to return to being one of the world's top two economies in the next 50 years, it must deepen and widen the reforms it began three decades ago.