Pakistan Among Hottest Mobile Banking Markets

Spurred by a favorable regulatory and technology environment, Pakistan is witnessing dramatic growth in branchless banking, according to a March 14, 2012 report by the State Bank of Pakistan.

Here are some of the key indicators contained in the State Bank report:

1. Number of branchless banking accounts jumped 40 percent to 929,184 in October-December 2011 (Second quarter of FY2011-12) from the preceding three month period.

2. Total amount of branchless banking deposits surged 169 percent to Rs 503 million in Oct-Dec 2011 from July-September 2011.

3. Number of branchless banking transactions during the second quarter rose 30 percent to 20.6 million while the value of transactions showed a growth of 35 percent to reach Rs. 79,410 million.

4. Branchless banking agents network in Pakistan grew by 16 percent in the second quarter (October- December 2011) of current fiscal year 2011-12 to reach 22,512 agents covering the entire length and breadth of the country.

5. The average size of branchless banking transaction was Rs 3,855 while the average number of daily transactions was 228,855.

6. Bills payment and mobile phone SIM card top-ups remained the dominating activity in the quarter under review with 53 percent share in total number of transactions, followed by fund transfers and deposits with share of 39 percent and 8 percent respectively.

7. While P2P payments remained the most popular mechanism with 74pc share in the total funds transfer, mobile branchless banking is penetrating all areas of payments such as utility bills, Government-to-Person (G2P) and Person-to-Person (P2P) payments while scaling up other services relating to deposits and loans.

A 2011 report by World Bank's Consultative Group to Assist the Poor (CGAP) describes Pakistan's mobile banking as "a unique laboratory for innovation". Here's an excerpt from it:

"Branchless banking regulation was first introduced in Pakistan in April 2008. From the beginning, the State Bank of Pakistan (SBP) has taken a constructive regulatory approach by providing clear guidance and being willing to listen to businesses and adjust regulation where necessary. A variety of business models is emerging that involves a wide range of players, including mobile network operators (MNOs), technology companies, and even a courier business. (Notably, a bank remains ultimately liable to SBP in all the models.) The government is further encouraging innovation by piloting the use of branchless banking to distribute government payments. Taken together, these factors make Pakistan a unique laboratory for innovation."

In a country where only 22% of the population owns bank accounts and more than 62% owns mobile phones, mobile banking is proving to be the fastest way to promote financial inclusion considered by experts to be essential to lift people out of poverty. Benefits include easy access for rural customers to banking services through agents in villages without bank branches, better documentation of the economy, enlarging of the tax-base and efficiency of economic transactions.

Related Links:

Haq's Musings

Pakistan Ranks High in Microfinance

Media & Telecom Sector Growing in Pakistan

Pakistan's Financial Services Sector

Fighting Poverty Through Microfinance

IBA on Entrepreneurship in Pakistan

Floods Dampen Enthusiasm on Pakistan Independence Day

Here are some of the key indicators contained in the State Bank report:

1. Number of branchless banking accounts jumped 40 percent to 929,184 in October-December 2011 (Second quarter of FY2011-12) from the preceding three month period.

2. Total amount of branchless banking deposits surged 169 percent to Rs 503 million in Oct-Dec 2011 from July-September 2011.

3. Number of branchless banking transactions during the second quarter rose 30 percent to 20.6 million while the value of transactions showed a growth of 35 percent to reach Rs. 79,410 million.

4. Branchless banking agents network in Pakistan grew by 16 percent in the second quarter (October- December 2011) of current fiscal year 2011-12 to reach 22,512 agents covering the entire length and breadth of the country.

5. The average size of branchless banking transaction was Rs 3,855 while the average number of daily transactions was 228,855.

6. Bills payment and mobile phone SIM card top-ups remained the dominating activity in the quarter under review with 53 percent share in total number of transactions, followed by fund transfers and deposits with share of 39 percent and 8 percent respectively.

7. While P2P payments remained the most popular mechanism with 74pc share in the total funds transfer, mobile branchless banking is penetrating all areas of payments such as utility bills, Government-to-Person (G2P) and Person-to-Person (P2P) payments while scaling up other services relating to deposits and loans.

A 2011 report by World Bank's Consultative Group to Assist the Poor (CGAP) describes Pakistan's mobile banking as "a unique laboratory for innovation". Here's an excerpt from it:

"Branchless banking regulation was first introduced in Pakistan in April 2008. From the beginning, the State Bank of Pakistan (SBP) has taken a constructive regulatory approach by providing clear guidance and being willing to listen to businesses and adjust regulation where necessary. A variety of business models is emerging that involves a wide range of players, including mobile network operators (MNOs), technology companies, and even a courier business. (Notably, a bank remains ultimately liable to SBP in all the models.) The government is further encouraging innovation by piloting the use of branchless banking to distribute government payments. Taken together, these factors make Pakistan a unique laboratory for innovation."

In a country where only 22% of the population owns bank accounts and more than 62% owns mobile phones, mobile banking is proving to be the fastest way to promote financial inclusion considered by experts to be essential to lift people out of poverty. Benefits include easy access for rural customers to banking services through agents in villages without bank branches, better documentation of the economy, enlarging of the tax-base and efficiency of economic transactions.

Related Links:

Haq's Musings

Pakistan Ranks High in Microfinance

Media & Telecom Sector Growing in Pakistan

Pakistan's Financial Services Sector

Fighting Poverty Through Microfinance

IBA on Entrepreneurship in Pakistan

Floods Dampen Enthusiasm on Pakistan Independence Day

Comments

In a move that would help spur the already booming development of IT content, Pakistan has beaten off competition from regional countries to bag World Bank’s contract for setting up a research lab for mobile software development including apps, The Express Tribune has learnt.

Pakistan Software Export Board – the agency tasked with the implementation of the project – has not made any official announcement, however, a well informed official told the Express Tribune that World Bank approved $380,000 in grants to Pakistan in November 2011 for a two-year project, mLab South Asia, to be set up in Lahore.

World Bank’s division InfoDev planned to establish five mobile software development research labs across the world including one in the Saarc region, the official said. India and Sri Lanka were also shortlisted for the region but Pakistan was picked as the final destination.

The business plan focuses on combining arts and science schools under the umbrella of PSEB. “We proposed that we will bring these two communities together for content-based applications,” a PSEB official who requested anonymity. “Our plan inspired them and we won the grant to set up the lab, he added.

PSEB is leading the project while Indus Valley School of Arts and Architecture, National College of Arts, and University of Engineering and Technology (UET) are among the implementation partners, the official said. The lab will be setup at UET, he added.

The purpose of the project is to establish mobile labs as specialised business incubators supporting mobile technology entrepreneurs, application developers and innovators, said infoDev Senior Communications Officer Angela Bekkers in an e-mail.

Bekkers said the grant comes from a Finland-financed trust fund, managed by infoDev, a global partnership programme in the World Bank. InfoDev’s mission is to enable innovative entrepreneurship for sustainable and inclusive growth, she added.

The blue print of the project is ready, according to PSEB official, and WB has already released the first year installment of $240,000 to PSEB earlier this year. The paper work is complete, courses have been designed, events have been planned for tech and art people, he said. The project will be executed after PSEB disburses funds to implementation partners. Pakistan Software Export Board did not respond to email queries sent by The Express Tribune.

http://tribune.com.pk/story/354211/software-development-lab-pakistan-beats-india-and-sri-lanka-to-get-contract/

In India the Mobile Banking Market is of a very recent origin, yet it has grown right since the concept was introduced. The Indian market can be divided into 2 segments: Urban and Rural. The Urban mobile banking segment has shown tremendous amount of growth, yet has scope for improvement in the field of payment transaction. According to many surveys conducted, majority of the customers in the Urban Segment widely use the mobile banking service for checking of account information and balances. The Rural mobile banking segment has also been targeted and the market is fairly new, yet there has been good amount of growth and awareness.

Find more Mobile Banking in India

..Wayne Beeson, supporter of Expeditionary Economics and other entrepreneurial economics initiatives, spotlights and recommends in his blog the entrepreneurship-based Expeditionary Economics model for Pakistan and similar countries to stimulate and sustain economic growth. He explains that Expeditionary Economics was put forth by The Kauffman Foundation in 2010 as an alternative to the largely ineffective international economic development policies of the U.S. State Department for the purpose of developing economic growth in areas where the U.S. is involved in counterinsurgency missions or disaster relief. Economic growth is vital for the stability of countries challenged by war and disaster. Mr. Beeson agrees with The Kauffman Foundation that entrepreneur-led economies are a proven model for developing economic growth.

“Entrepreneurship positively impacts the economic well-being of individuals, families, and nations, and Expeditionary Economics recommends entrepreneurship as the foundation of our international economic development policy and endeavors,” says Mr. Beeson. He notes that Professor Looney’s study on applying Expeditionary Economics to the economy of Pakistan to stimulate economic growth is not only a model for Pakistan, but also a model for other countries facing similar challenges.

“Professor Looney’s study is the beginning of a plan of action to systematically implement entrepreneurial activity in a distressed economy in which the U.S. is committed to providing assistance for various reasons. If the U.S. can be successful in helping create prosperous, self-reliant economies, it is a win-win outcome. I individuals, families and nations prosper and support democratic reforms where the people of a country own their own economy and government, and the U.S. wins by having friends in the international community who support rather than threaten U.S., because they support our values and ideals,” explains Mr. Beeson.

Professor Looney’s paper can be downloaded at expeditionaryeconomics.org., or from this news release.

Read more: http://www.timesunion.com/business/press-releases/article/Wayne-Beeson-Recommends-Expeditionary-Economics-3437021.php

Pakistan Post has launched an Electronic Money Order (EMO) service at seventeen centres in ten districts of the country on Monday. The service has been initiated with an investment of Rs500 million in a centralised software system, without taking the network of competitors doing business in this field into account, The Express Tribune has learnt.

Out of total funds, Pakistan Post has provided Rs100 million to vendor Telconet, who has installed the system and will supervise it, an official said.

Although the service has been initially launched at seventeen locations in 10 different cities, the investment on the system is difficult to justify, the official added. Service charges are comparatively low, as compared to the Easypaisa and UBL Omni services, but the network offered by Pakistan Post cannot beat that offered by its competitors, he maintained.

For a transfer of Rs10,000, Pakistan Post’s charges are Rs160 less than charges received by competitors, the official added. The whole service, he claimed, is based on the very innocent assumption that the customer considers only service charges, while ignoring the time factor and load on the system. “It seems that no cost-benefit analysis has been carried out, and that the lower prices will only translate into lost revenue. The service should have been competitive in all respects: including service charges, availability of service, available timings and the quality of service,” he added.

Easypaisa is currently providing a similar service at 52 branches of the Tameer Bank, 100 walk-in centres, 750 Telenor franchises, and 10,500 merchants countrywide; while UBL Omni is also providing a similar service at more than 600 locations in the country.

“If I have to collect, say, Rs10,000 from the Lahore General Post Office (GPO), I’ll have to travel more than an hour – all the way from Wapda town to Mall road – and spend nearly Rs200 worth of fuel. I would rather prefer to collect this amount at a point nearest to me, saving both time and money,” Muhammad Imran a customer at the Lahore GPO, told The Express Tribune.

Another point to consider is the system itself, and the marketing strategy employed. The Easypaisa system utilises the cell phone network. All Easypaisa merchants and service centres use mobile phones to carry out a transaction, whereas the system available to the Pakistan Post is based on desktop computers and a virtual private network system. This equipment requires uninterrupted power supply, a difficult-to-meet requirement in times of heavy load-shedding.

http://tribune.com.pk/story/434461/up-and-coming-google-pakistan-earns-500-million-in-revenue/

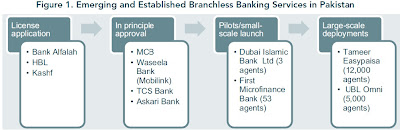

KARACHI: In another strong sign that branchless banking is gaining momentum in Pakistan, Zong and Askari Bank – the latest entrant to join this bandwagon – have partnered to launch a complete branchless banking solution.

The State Bank of Pakistan (SBP), according to sources in Zong, issued branchless banking licence to Zong and Askari Bank last Friday after auditing their pilot project, launched in May this year.

This is the second branchless banking license issued by the SBP this month – the central bank had awarded a mobile financial services licence to Mobilink’s sister concern Waseela Bank.

The product, according to Zong officials, will soon be launched commercially. The branchless banking portfolio includes services like mobile account, money transfers, utility bill payment among others, Zong said in a press statement. Additionally, Zong is going to offer services like salary disbursement, it added.

This will be first of its kind collaboration where a telecom operator and a commercial bank will provide branchless banking services under a relationship where none of the parties has any shares or controlling interest in each other, – the revenue will be shared between the partners.

“Branchless banking is only the beginning of a new banking revolution in the country, we are launching our new branchless banking services to foster financial inclusion of the unbanked population in Pakistan,” Usman Ishaq, executive director (commercial) at Zong said while responding to an email by The Express Tribune.

The project, according to Ishaq, is targeted for the unbanked population of the country, who have no means of availing banking or financial services.

It merits mentioning that only 22% of the country’s population owns a bank account; by contrast, more than 60% Pakistanis have access to mobile phones – the unbanked segment of Pakistan, therefore, provides an opportunity for expansion of branchless banking.

Branchless banking regulation was introduced in Pakistan in April 2008; the central bank has, since then, taken a constructive regulatory approach to encourage investment in this sector – the SBP had issued four branchless banking licences between 2008 and 2011 and the branchless banking just clicked in the country.

Telenor Pakistan, through its subsidiary, Tameer Microfinance Bank launched easypaisa in October 2009 – they processed 23 million transactions amounting to Rs43 billion ($500 million) till the end of July, 2011.

In April 2010, United Bank (UBL) entered sector by launching UBL Omni. It got numerous contracts to disburse payments for public sector organisations and government schemes such as the Benazir Income Support Programme, flood relief programme and the United Nations World Food Programmme.

First MicroFinance Bank and Dubai Islamic Bank Pakistan were among the pilot or small-scale launches – the former had partnered with Post Office in 2008 for loan disbursements.

The fast growing branchless banking sector of the country even got attention from international researchers.

In an October 2011 report – Branchless Banking in Pakistan: A Laboratory for Innovation – Consultative Group to Assist the Poorest (CGAP) mentioned Pakistan as one of the fastest growing markets for branchless banking in the world.

In its report, the CGAP had mentioned Waseela Bank, Askari Bank, Bank Alfalah and MCB Bank as anticipated players to enter the market during next 12 months. While the first two have already got licences, the others are yet to announce their entry in this growing market segment, if they still intend to that is.

http://tribune.com.pk/story/468247/as-mobile-banking-grows-zong-askari-bank-join-the-race/

The overall value and volume of e-banking transactions throughout the country increased during the second quarter (October to December 2012) to Rs 7.6 trillion (18.02 per cent)and Rs 79.45 (11.31 per cent) million respectively, the State Bank of Pakistan reported on Wednesday.

State Bank of Pakistan’s Payment Systems report for the second quarter of FY13 released today revealed that the branches of 484 banks in Pakistan were added to the Real-Time Online Branches (RTOB) network during the second quarter of the current fiscal year (FY13) and now 94 percent branches are offering online banking services.

Calculating the overall internet banking services across the country, overall 9,896 branches of banks out of 10,523 are offering the service. During the second quarter, the overall value and volume of internet banking transactions had seen an increase in of 18.82 percent and 14.29 percent in the overall value and volume of internet banking from the first quarter of 2012, respectively.

The Payment Systems infrastructure in the country had also seen an increase because of the installation of 245 new Automated Teller Machines at banks around the country. Today, the number of ATMs across Pakistan has reached a total of 6,232. The report further said that ATM transactions had a major share of 61.12 percent in terms of transaction volume with an average value of Rs9,779 per transaction.

The overall e-banking transactions in value terms was 6.27 percent during the second quarter, increasing the value and volume of ATM transactions by 10.33 percent and 10.68 percent respectively in the second quarter as compared to the first quarter of the current fiscal year.

The report also said that over 20.72 million banking cards were issued in the country by the end of December, 2012, witnessing an increase of 5.33 percent in the second quarter compared to the preceding quarter.

Point of Sale (POS) terminals showed a growth of 6.25 per cent and 5.06 per cent in value and volume respectively as compared to the first quarter of the current fiscal year, with value and volume of transactions standing at Rs22.1 billion and Rs4.5 million, respectively, in the second quarter.

The report also pointed out an increase of large-value payments through Real Time Gross Settlement (RTGS) with 9.46 percent in value and 10.35 percent in volume as compared to the first quarter. The recorded value and volume was Rs42.13 trillion and Rs12.16 billion respectively in the second quarter.

The report also revealed that major portion for the increased number of overall Pakistan Real Time Interbank Settlement Mechanism (PRISM) transactions increased 14.06 percent during the same period, which was contributed by Interbank Funds Transfers (IBFT). Similarly, the value of overall PRISM transactions increased by 14.96 percent due to securities settlement.

http://tribune.com.pk/story/506723/e-banking-transactions-cross-rs7-trillion-state-bank/

A shared mobile money network, built on Visa's Fundamo technology, that can be tapped by banks and telcos is preparing to launch in Pakistan.

Monet - which was set up by the massive Abu Dhabi Group last year - has now secured approval from the State Bank of Pakistan to build its network, which is being offered to local firms planning to launch mobile money services.

Built on Fundamo technology, Monet says its offering will provide a managed service platform, agent management services and bill aggregation services to new financial institutions and network operators interested in entering branchless banking services.

The first clients are Pakistan's sixth largest financial institution, Bank Alfalah, and Warid Telecom, who have teamed up to launch a new brand on the platform.

Monet says that its network will make it cheaper, easier and quicker for firms to tap into Pakistan's huge unbanked market. According to the Pakistan Access to Finance Survey, only 12% of the population has access to formal financial services, yet mobile penetration stands at nearly 70%, says the Pakistan Telecommunications Authority.

A recent study by the Boston Consulting Group estimates that 35% of the country's adult population will be using mobile financial services by 2020.

Ali Abbas Sikander, CEO, Monet, says: "We are building an open and collaborative eco-system which benefits all the stakeholders of the financial services ecosystem in Pakistan. Collaborative mobile financial services, as opposed to bank-led or telco-led deployment, is the paradigm shift which will assist in creating a bigger and less costly enabling environment for the issuers, acquirers and service providers."

Aletha Ling, COO, Fundamo, adds: "The platform allows service providers to think big, start small and scale fast. The result will be an ecosystem that that will support the long term and sustained growth of the Pakistani mobile financial services market."

http://www.finextra.com/News/FullStory.aspx?newsitemid=24626

...The central policy objectives of SBP are to ensure safety, soundness and efficiency of the banking system, and to protect the interest of consumers, he said, adding that since branchless banking is becoming a vital component of the national payment grid, it is prudent for all stakeholders to ensure that appropriate measures are in place to mitigate inherent risks associated with it like access by unauthorised persons or criminals such as hackers, money launderers, terrorist financiers etc.

He said being fully cognisant of the risk factors involved in such unconventional modes of banking, SBP has been proactively monitoring developments and associated risks both at system and entity level in order to take appropriate corrective measures in a timely manner.

The SBP governor said that branchless banking has also proved to be an effective instrument in channelising the government to persons (G2P) payments in trying times like serving internally displaced persons (IDPs), and devastating floods for the last two years. The Benazir Income Support Programme (BISP) beneficiaries are also being served effectively through the same mechanism, he said, adding that In the coming days, this channel is expected to continue playing an important role towards the promotion of financial inclusion and the management of G2P programmes like salaries disbursements, pensions, BISP, Watan Cards, Pakistan Cards and tax collections services, etc. The existing branchless banking deployments can cater to the needs of over 10 million potential beneficiaries of G2P payments in Pakistan, he added.

Anwar said that four branchless banking models including Easy Paisa, Omni, Mobile Cash and Time Pey are fully operational while two are running live pilots. He said that the branchless banking current growth trajectory is expected to get further steeper in the years ahead.

He said that the number of agent network servicing branchless banking customers has reached 42,000. Therefore, the basic financial services can now be accessed in the remotest parts of the country through any of these agents. Approximately 194 million transactions worth Rs 813 billion and more than 2.0 million m-wallets have been opened till date, he said, adding that numbers will improve significantly. The infrastructure of payment systems and branch network is also showing an increasing growth trend, he said adding that the ATMs network has increased to 6,232 whereas branch network has reached 11,600 while 94 percent of our branches are now real time on-line. Similarly, the number of plastic cards has increased to 20 million and the number of POS machines has increased to 34,000 units. This is a significant achievement, and this also demonstrates the opportunity to bring the benefits of this infrastructure to millions of the unbanked population, he added.

While acknowledging that branchless banking has gained critical mass in a short period of time, the SBP governor was of the view that the market has to start shifting transactions from first generational services (person-to-person/bills payments) to second generational services (account-to-account and inter-bank transfer). The players need to expand their product portfolio by offering new products and services for their target market. In my view, this is part of an inevitable evolution which will ensure the long-term sustainable development of the sector, encourage micro savings and help in meeting the demands for inclusive financial services of the target market, he added.

http://www.dailytimes.com.pk/default.asp?page=2013\03\15\story_15-3-2013_pg5_1

http://on.wsj.com/1MTSnCw

Telenor Pakistan is one of the country’s first mobile banking programs making financial services available to millions of Pakistanis. Photo: Telenor Pakistan

Pakistan has a great opportunity to become more ambitious in reforming its economy so that more people are lifted out of poverty more quickly and prosperity is more widely shared among its people, said World Bank Group (WBG) President Jim Yong Kim.

Noting that the government had stabilized the economy over three tough years, Kim said he had discussed in meetings with the prime minister and finance minister about the importance of pressing forward with reforms that would unlock the country’s potential. As part of the World Bank’s continued support to the country, there was discussion of a Development Policy Credit to promote economic reforms.

“Now is the moment for Pakistan to step up to a higher level of growth and opportunity for all its people,” said Kim. “In my meetings with the prime minister and finance minister, we discussed going to a higher level of ambition for reforms for the economy. These could include strengthening the role of the private sector for job creation, accelerating energy reforms, making improvements at the community level for health and education, and ensuring that anti-poverty measures are effective at reaching poor people.”

Kim made his comments on the first day of his two-day visit to Pakistan after meetings in Islamabad with the government leadership, including economic ministers and secretaries from provincial and federal governments.

Kim participated in a State Bank of Pakistan launch event for WBG support to Pakistan’s financial inclusion reform agenda, “Pakistan’s Path towards Universal Financial Access.” “The National Financial Inclusion Strategy has come at a particularly opportune moment as new technology and the rapid expansion of branchless banking offer unprecedented opportunities to transform financial inclusion in Pakistan. Pakistan is now leading the way in South Asia when it comes to digital finance and branchless banking”, said Kim.

The UN Secretary General’s Special Advocate for Inclusive Finance for Development, Queen Máxima of the Netherlands, and Finance Minister Ishaq Dar also participated in the event.

Kim also participated in a panel discussion on “Managing Displaced Populations” and learnt how the country managed a large Afghan refugee population. The event was co-organized by the World Bank, the Economic Affairs Division and UNHCR, in the context of the continuing global refugee crisis.

“There is much the world can learn from Pakistan, which has for decades hosted refugees from other countries or had to cope with temporarily displaced people within its own borders,” said Kim. “We are committed to support the Government of Pakistan in repatriating the crisis affected displaced people through the newly effective cash transfer project.”

Later in the day, he met with the provincial leadership of Khyber Pakhtunkhwa and Punjab and learned about province-level reform efforts and development projects under implementation and preparation with World Bank Group support. He underlined the importance of the role of the provincial governments in the effective implementation of reforms.

Kim later plans to meet private sector representatives, students, and the provincial leadership of Sindh.

The World Bank Group in Pakistan:

The World Bank’s program in Pakistan is governed by its Country Partnership Strategy (CPS) agreed with the government. The World Bank Pakistan portfolio has 26 investment lending projects under implementation with a total net commitment of $4.99 billion. To date, we have committed over $5.6 billion in Pakistan, including $1.2 billion during the 2015 fiscal year. IFC’s advisory services program in Pakistan is one of its largest in the region, with 13 active projects and a funding commitment of over $20 million